Brandon Bell

Brandon Bell

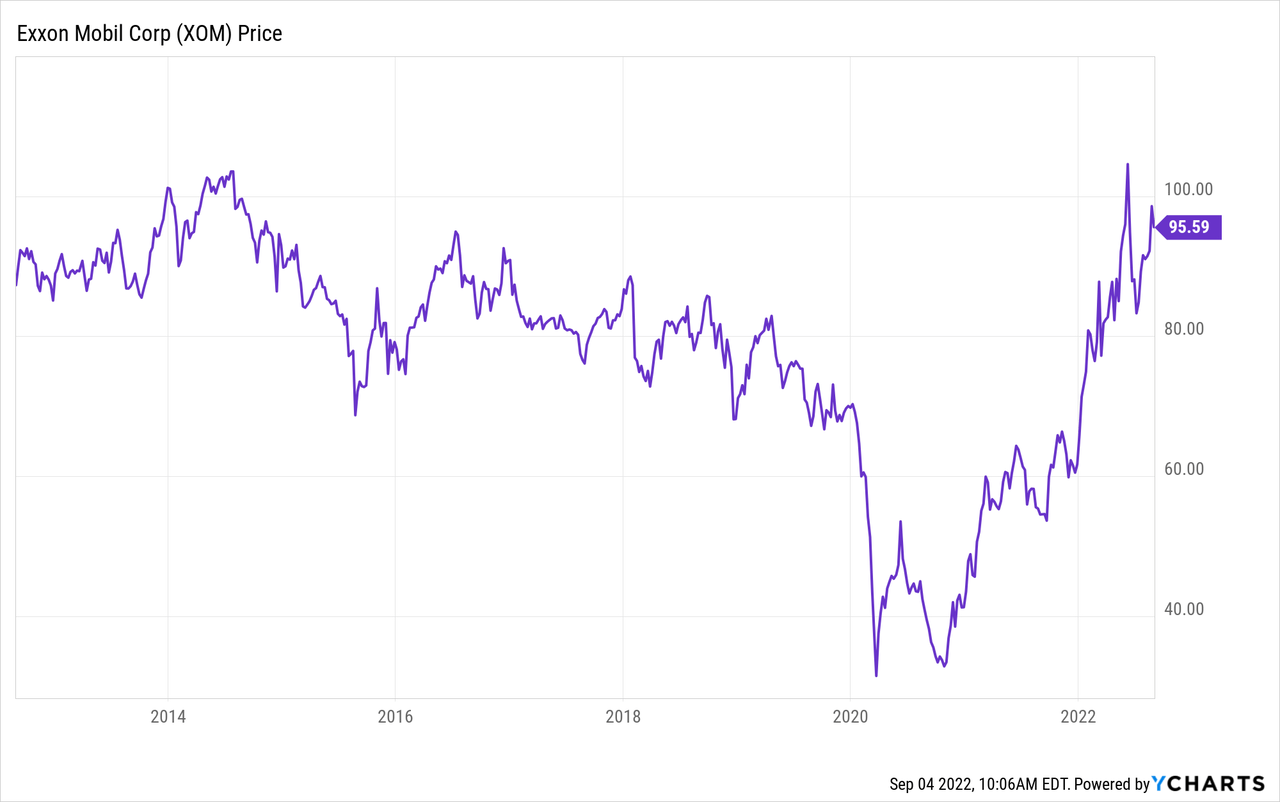

Integrated international oil company Exxon Mobil (NYSE:XOM) has been a perennial under-performing energy company for well over a decade (see chart below). That has been very painful for long-term shareholders like myself that got used to the days when Exxon enjoyed the reputation as being one of the most well-run and efficient energy companies on the planet. Enter hedge fund and activist group Engine #1. As most of you know, Engine #1 shocked the energy industry when it fought a well-organized battle against Exxon and won not one, not two, but three seats on Exxon’s board-of-directors in a rather impressive move on the company. While many shareholders wrung their hands over the “invasion of the greenies”, they obviously did not understand the totality of Engine #1’s mission (which I will discuss below). For me, and for many institutional investors, Engine #1 has been a Godsend that has practically rescued Exxon from the debts of mediocrity (to put it nicely). As a result, today I am more bullish on Exxon than I have been in well over a decade.

Note that Exxon’s stock today is roughly where it was 10-years ago, a period that included the biggest bull-market of our lives and during which Brent oil made multiple trips above $100/bbl.

As mentioned previously, in June of last year tiny Engine #1 – with only a 0.02% stake in Exxon stock – sent shock-waves through the energy sector when it won three seats (out of 11) on Exxon’s board of directors. New members Gregory Goff, Kaisa Hietala, and Alexander Karsner are all former energy executives who have added much needed energy expertise to Exxon’s board. Both Hietala and Karsner have significant experience in renewable energy while Anders Runevad, Engine #1’s fourth nominee and former CEO of wind power company Vestas (OTCPK:VWDRY), did not get elected.

Despite the false narrative that “greenies” were taking over the company and will wreck it, informed shareholders and investors took note of what #1’s two primary objectives actually were:

#1: Refresh the Board of Directors with energy experience.

#2: Impose greater long-term capital allocation discipline.

As a long-suffering Exxon shareholder, I certainly supported those two objectives. And, despite last minute personal phone calls by CEO Wood, so did institutional investors like Vanguard, Blackrock, and State Street who were very concerned about Exxon’s lack of shareholder returns as well as the company’s seemingly inability to come to grips with the reality and risks associated with global warming.

The battle over board nominees between Exxon and Engine #1 was nicely summarized an article featuring professor Witold Henisz of the University of Pennsylvania’s Wharton School: see Why Engine #1’s Victory Is A Wake-Up Call For Exxon Mobil And Others. This is a must-read for all Exxon shareholders.

In my opinion, Engine #1’s impact on Exxon has been nothing but positive for ordinary and institutional shareholders. Let me explain.

In May, Engine #1 published an article summarizing the changes in Exxon since it won the three board seats: see ExxonMobil: One Year Later. This is another must-read for all Exxon shareholders.

Note the big changes in Exxon since Engine #1 entered the fray – some of which the company made soon after Engine #1 went public with its intentions:

As Engine #1 pointed out:

Exxon destroyed more than $170 billion in shareholder value through poor capital allocation over the past decade prior to our campaign. As recently as last year, the Wall Street Journal reported, Exxon “had been unable to fund its dividends through free cash flow alone even in 2019 before the pandemic.

Exxon’s previous strategy, which I have previously characterized on Seeking Alpha its intent to “get bigger just for the sake of getting bigger” (regardless of the total returns for shareholders … was great for the executive management team but terrible for shareholders. Indeed, CEO pay zoomed 30% higher even though returns over a decade were actually negative.

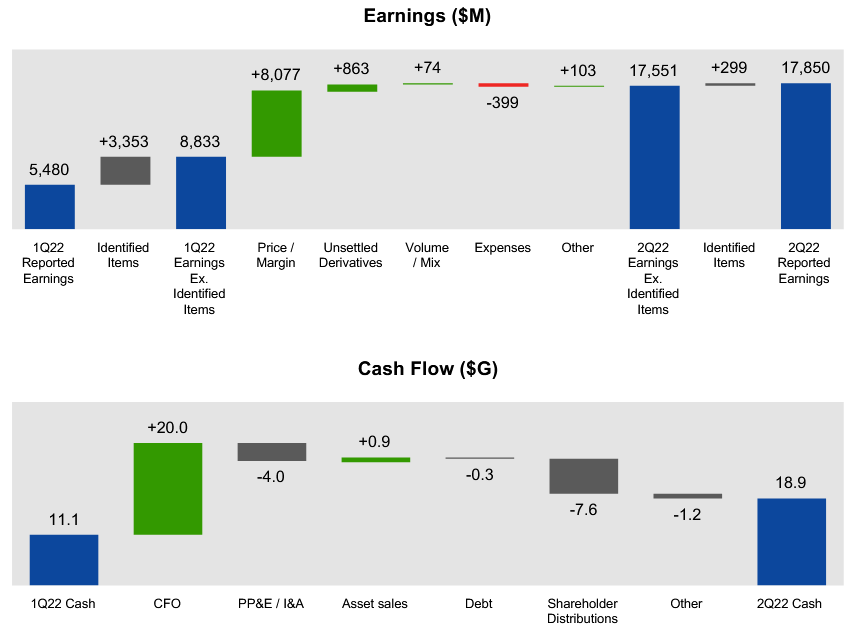

As a result of these changes, Exxon’s Q2 EPS report was much better than it otherwise would have been. Highlights included:

Exxon

Exxon

No doubt Exxon benefited from strong global O&G prices as a result of a general covid-19 recovery and Putin’s horrific war-of-choice on Ukraine and the resulting sanctions placed on Russia by the United States and its Democratic & NATO allies. However, investors should note another very positive change: Exxon’s year-to-date cap-ex was only $9.5 billion, or roughly half of what was planned prior to #1’s campaign.

Also, note that Q2 was a relatively weak quarter for Exxon’s chemicals margin, but strong natural gas pricing more than made up for it.

This new-found capital discipline has enabled Exxon to pay down more than $20 billion in debt to bring debt levels back inline to pre-pandemic levels. As a result, XOM recently announced it had tripled its repurchase plan for up to $30 billion of Company shares through 2023. This represents Exxon’s first meaningful share repurchase program since 2010.

Another meaningful change since Engine #1’s campaign and Exxon’s resulting decision to drop its 25% production growth target by 2025, is that Exxon is, finally, starting selling a significant number of non-core and low-margin assets. Here are some examples just this year:

All these agreements and developments are arguably an acceleration of Exxon’s traditional asset sales history and are, in my opinion, a very much needed and long overdue effort to high-grade its portfolio. This is great news for Exxon’s ordinary shareholders because it will raise Exxon’s overall efficiently, lower the company’s breakeven point, enable additional debt reduction, and allow the company to focus its attention on key upstream assets like the Guyana and the Permian. At the end of the day, it should lead to much better total returns for shareholders (after all, how could they be worse than the last decade or so?).

Also, in January of this year, Exxon announced it would consolidate its headquarters in Houston, TX as part of a planned reorganization that would leave it with three business units:

Exxon said the moves would lead to more than $6 billion in structural cost savings by 2023, which begs the obvious question: why hadn’t this reorganization been done much earlier? Regardless, the reorg is yet another sign that Exxon has become much more focused on efficiency and lowering its breakeven point.

And finally, we get to Engine #1’s third priority:

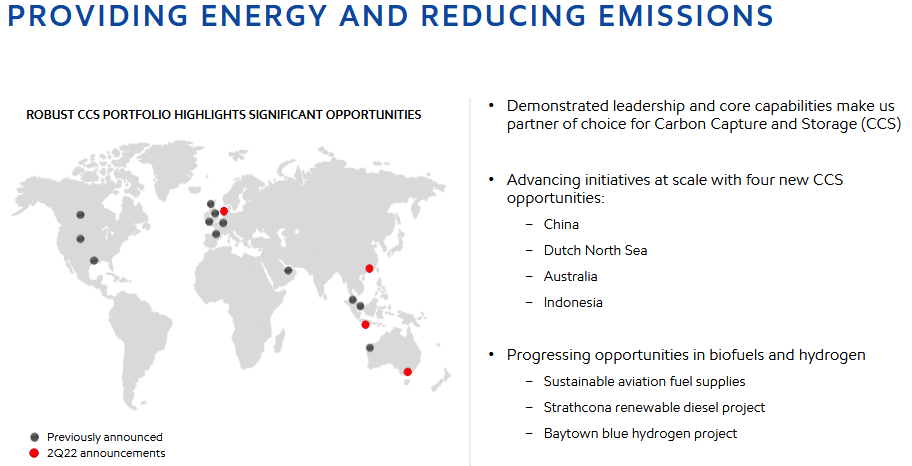

#3: Implement a strategic plan for sustainable value creation in a decarbonizing world.

Engine #1’s goal here is for Exxon to come to grips with the reality of global warming and better prepare itself for the age of EVs and a clean-energy future by reducing emissions and investing in low-carbon solutions:

Exxon

Exxon

Indeed, Exxon has pledged to spend $15 billion on low-emissions projects by 2027. Personally, I would like to see Exxon start making direct investments in solar, wind, and battery storage capacity. Perhaps when more investors finally understand the significant positive impact Engine #1 has had on Exxon so far, they will be more supportive next go-around and place more #1 nominees on Exxon’s board. I know I will certainly would vote for Engine #1 nominees. That’s because, so far, Engine #1’s impact on Exxon has been nothing less than a very positive transformation that has Exxon much better positioned for the future.

Meantime, Exxon’s turnaround will be led by its production shift toward liquids as its high-margin upstream jewels, Guyana and Permian, will be ramping up over the coming years: Guyana to 850,000 bpd by 2027, and Permian to 800,000 boe/d by 2027. As a result of all these positive changes, Exxon’s breakeven point has been dropping and the company can now probably cover annual cap-ex and the dividend with Brent at ~$50/bbl.

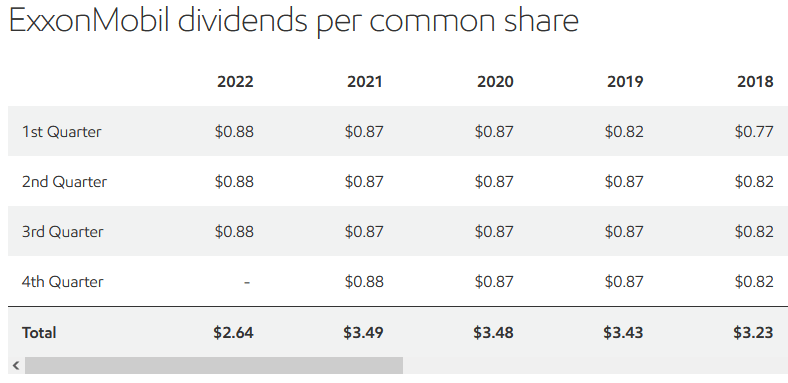

Due to Exxon’s unwise over-spend on large global petchem projects, combined with the covid-19 demand destruction, the company’s quarterly dividend growth has been anemic over the past few years, and was stuck on $0.87/share for 10 quarters before being raised by a paltry penny in Q4 of last year:

Exxon

Exxon

That’s obviously a dividend record in stark contrast to shale oil producers, who are currently falling all over themselves to pass on their free-cash-flow to shareholders in the form of base + variable dividends. Now that Engine #1 has helped rein-in Exxon’s capital expenditures and instituted some discipline to the company’s strategy, XOM shareholders should be able to look forward to higher dividends rewards in the coming years. However, with Exxon already announcing $30 billion toward share buybacks, it’s clear (at least to me), that the board feels the stock is undervalued and buybacks should be prioritized over dividends directly to shareholders. While I do agree the stock is undervalued, my followers know I am not a big fan of any company greatly over-emphasizing buybacks over the dividend. Note that Exxon’s current $0.88/share quarterly dividend was a Q2 quarterly obligation of $7.6 billion, or an annual obligation of an estimated $30.4 billion.

Today, Exxon is a vastly different company than it was prior to Engine #1’s campaign for seats on its board-of-directors. #1 got significant support from institutional investors for its primary goals of adding energy expertise to the board as well as increasing the company’s meager total returns. As a result, annual cap-ex is down by ~$10 billion, the balance sheet has been repaired, and the company’s portfolio is finally being significantly up-graded so as to focus on its highest return opportunities (i.e. Guyana and the Permian). As a result, Exxon is now much better positioned for the up- and down-cycles of the global oil & gas market.

Exxon stock currently trades with a P/E=7.5x and yields 3.7% and is a BUY based on its much-improved balance sheet, its free-cash-flow profile, and it’s much better strategy moving forward.

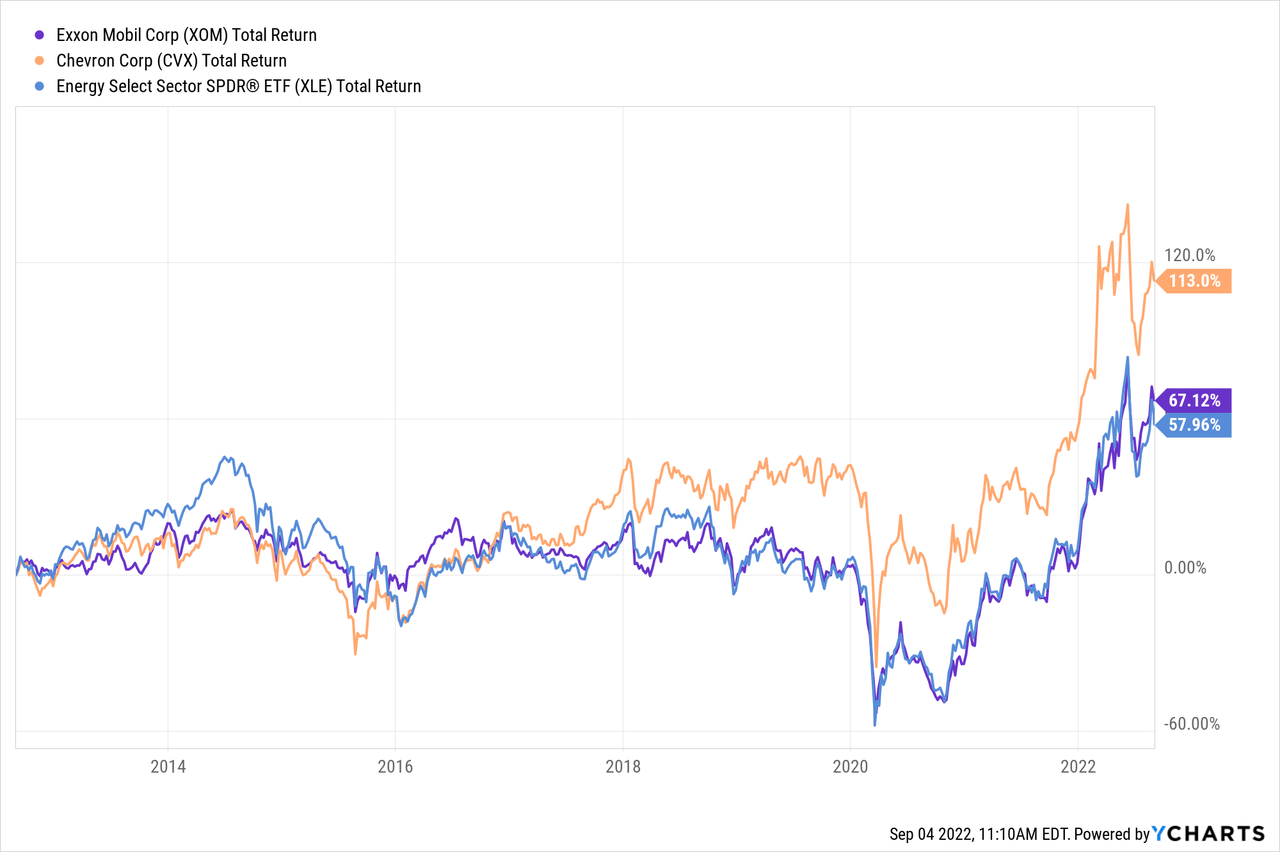

I’ll end with a 10-year chart of Exxon versus peer Chevron (CVX) and the broad energy sector as represented by the Energy Select Sector SPDR ETF (XLE):

As can be seen, Chevron – my preferred pick over Exxon – has been running rings around XOM for many years. However, with Engine #1’s influence, that trend may be starting to turn. I’m going to wait a couple more quarters before I change my opinion in favor of Exxon, but the company appears to be on-track to regain its crown as king of the international integrated oil companies. However, I doubt it ever would have happened without the very positive influence of Engine #1, and CEO Wood’s concerned that #1 could win even more seats on the board next go ’round if the company didn’t climb out of the ditch it was in.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of CVX, XOM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am an electronics engineer, not a CFA. The information and data presented in this article were obtained from company documents and/or sources believed to be reliable, but have not been independently verified. Therefore, the author cannot guarantee their accuracy. Please do your own research and contact a qualified investment advisor. I am not responsible for the investment decisions you make.