THE WOLF STREET REPORT

Imploded Stocks

Brick & Mortar

California Daydreamin’

Canada

Cars & Trucks

Commercial Property

Companies & Markets

Consumers

Credit Bubble

Energy

Europe’s Dilemmas

Federal Reserve

Housing Bubble 2

Inflation & Devaluation

Jobs

Trade

Transportation

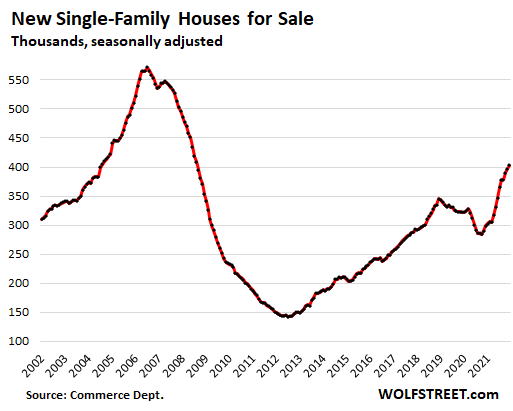

Homebuilders are on a wild ride, beset by shortages of materials and supplies, near-eternal lead times, spiking construction costs, difficulties in hiring, and projects that are bogged down. And inventories for sale, driven by homes that are still under construction and cannot be completed due to the shortages, are piling up.

Inventory of single-family houses for sale at all stages of construction has been surging throughout the year 2021 and in December hit 403,000 (seasonally adjusted), up 58% from a year ago, and the highest level since August 2008. This represents about 6 months’ supply, according to date from the Census Bureau today:

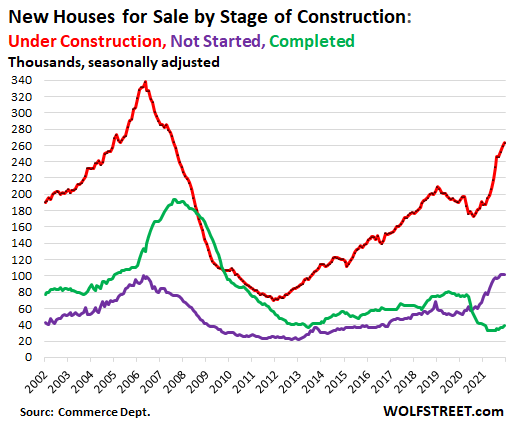

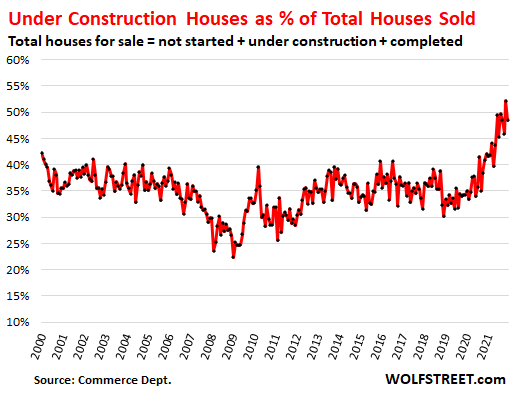

The number of single-family houses for sale that were still under construction jumped to 263,000 in December, the highest since August 2007 (red line in the chart below).

The number of houses for sale where construction hasn’t started yet remained at 101,000 in December. The past three months were all above 100,000, the highest in the data, having edged past the prior high of April 2006 (purple line).

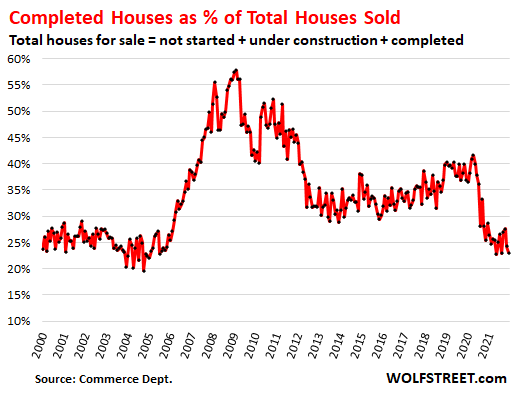

But the number of completed houses for sale has been bouncing along record lows in all of 2021, as builders face shortages that prevent them from completing the houses. These shortages range from windows to appliances. And once houses are completed – if they haven’t sold already during the prior stages – sell quickly. In December, 39,000 completed houses were for sale (green line).

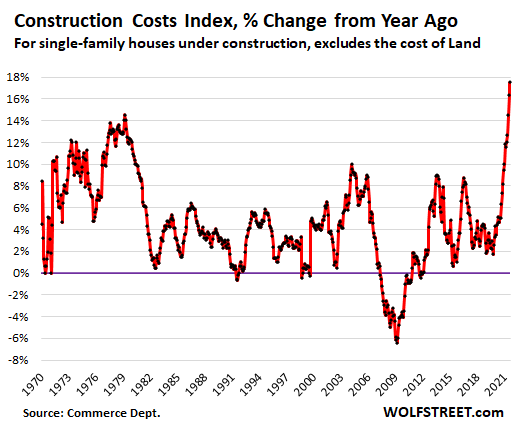

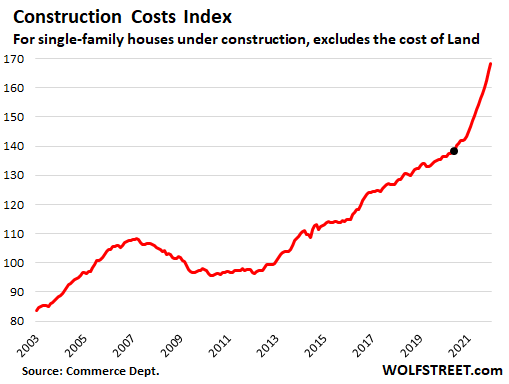

Construction costs of single-family houses spiked by 17.5% year-over-year in December, according to separate data from the Census Bureau today. This was the worst spike in the data going back to 1970. Compared to two years ago, construction costs are up 23.5%. These construction costs exclude the cost of land and other non-construction costs:

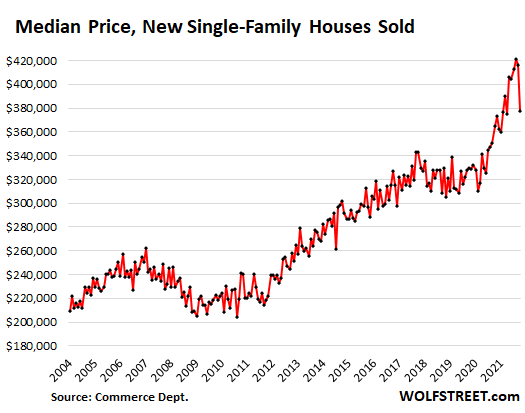

The median price of single-family houses sold in December plunged from $416,100 in November to $377,700 in December. This slashed the year-over-year price gains that had run in the 23% to 32% range since July to just 3.4%.

The median price is volatile and is skewed by changes in the mix of lower-priced homes versus higher-priced homes that sold that month. And there was some of that in December, with the number of houses sold in the $200,000 to $299,000 range rising and with the number of houses sold in the $400,000 and up categories falling, which shifted the mix.

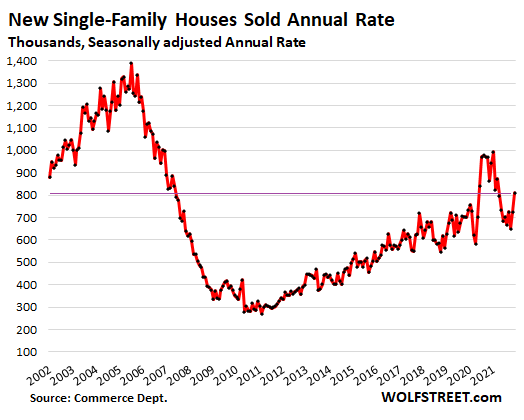

Sales of new single-family houses in December, at all stages of construction combined, rose from November, but was still down 14% from a year ago, to a seasonally adjusted annual rate of 811,000 houses. Sales remain far below the boom years of 2002-2006.

Apartment buildings and condo buildings are not included here, and the huge boom in multi-family construction in urban centers over the years is not reflected here. This is just sales of new single-family houses:

Sales of completed houses rose from November to a seasonally adjusted annual rate of 187,000 in December, but were still down by 31% both from December 2020 and from December 2019 as inventories of completed homes hovered near record lows, and there wasn’t much to sell.

The share of completed houses as a percent of total sales dropped to 23.1%:

Sales of houses under construction jumped to a seasonally adjusted annual rate of 393,000 houses in December, the highest in a year, as more buyers who couldn’t find a completed house ended up buying a house that was still under construction.

The share of under-construction houses as a percent of total sales backed off from the record high in November, to 48.5%:

Sales of houses where construction hasn’t started yet – customer buys a house that the homebuilder will then build for the customer – jumped to a seasonally adjusted annual rate of 231,000 houses.

The share of not-started houses as a percent of total sales jumped to 28.5%, just a little below the middle of the range since 2021:

What these charts are showing are the results of the massive distortions that have spread across the economy. The distortions include interest rates (now surging) that are still far below the rate of inflation; artificially stimulated demand for goods of all kinds leading to shortages and transportation chaos; and labor shortages of the type we haven’t seen before. So now there is lots of supply of new houses, but that supply is building up in the pipeline and much of it remains stuck there.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.![]()

Email to a friend

Hi Wolf,

Do you still think Jerome is serious about inflation and not willing to stay way behind the curve ?!

article coming.

Looking forward to it. I like to keep track of what this porker is up to. Oink, oink!

He did not raise the rates by even 0.25% when CPI inflation is running at 7% and real at 10+%. He did not even commit to raising rates in March if you paid attention. This when there is more than stable employment. How many times Fed need to scr ew common people before they get the message that Fed’s real mandate is to serve the elite and keep pumping the asset and stock bubble.

“A society becomes totalitarian when its structure becomes flagrantly artificial: that is, when its ruling class has lost its function but succeeds in clinging to power by force or fraud.” ~ George Orwell

“Construction Costs Spike 17.5%, Worst since at least 1965.”

Weimar Boy Powell informed us today that, soon, raising interest rates will be warranted. Not now, but soon. Then he’ll draw his pea shooter and start plinking away at inflation, which is fully armed with automatic weapons. Because, you see, Weimar Boy Powell really means business.

Luckily they’re continuing another month of asset purchases. Makes total sense. Absolutely. Definitely an inflation-fighting thing to do. There’s just no reason to stop purchases now. No, no way.

You have 6 more weeks to day trade. Including FED members!!!

” There’s just no reason to stop purchases now. No, no way.”

If that interpretation is accurate. To me it means the people that the FED happens to really be working for need another month to adjust their positions.

The FED does not work for the average Joe, we are just the designated bag holders.

Deja vu, all over again?

Look out below…

Apropos of near-eternal lead times:

So a man gets into a chat with god, and he asks him, “Lord, how long is eternity to you?”

And the Lord replies, “a second”.

And the man asks, “Lord, how much is a house worth to you?”

And the Lord replies, “a penny”.

So the man gets clever and asks, “Lord, may I have a penny?”

And the Lord answers. “Sure, wait just a second…”

May we all have the serenity to accept the things we cannot change…

Good one!

Brilliant!

Sorry it not in my Rebellious nature to bend over and take it up the a$$. That’s whats wrong with this country everybody is to passive. The maases are like sheep being led to the slaughter.

“Our countrymen have all the folly of the ass and all the passiveness of the sheep.” ~ Alexander Hamilton

“I prefer dangerous freedom over peaceful slavery.” ~ Thomas Jefferson

“Liberty is not for these slaves; I do not advocate inflicting it against their conscience. On the contrary, I am strongly in favor of letting them crawl and grovel all they please before whatever fraud or combination of frauds they choose to venerate…Our whole practical government is grounded in mob psychology and the Boobus Americanus will follow any command that promises to make him safer.” ~ H. L. Mencken

Weimar Boy Powell and his buddies are going to bury the President. The rage that this high inflation is causing will be directed towards this administration. Powell just told us today that he will not be taking inflation seriously.

Yes, but the politicians are still economic illiterates and so are most of the voters who elect them.

Being in the majority, the democrats want to “do something” about inflation but this doesn’t include cutting off the “free money” spigot which is contributing mightily to it.

He works for those who own the banks that own the FED.

Inflation is GOOD for the owners.

Massive Debt is GOOD for the owners.

He is doing his job.

I for one would love to see that under construction number rise dramatically as we move throughout the year. Let all of these builders see their profit margins drop to nothing if they eventually have to start dropping prices because interest rates rise above 4.5% in the next 12 months.

Not sure if it’s true, but I hear there are a ton of apartments being constructed in population in flow areas of US.

It’s possible but not likely. The construction industry is a FOR PROFIT industry. If margins drop, housing starts will drop. I build and I stopped temporarily last year when lumber producers started gouging their clients by raising prices over 500% while at the same time paying THIER suppliers rock bottom prices that dated back to 2011

This is why home prices are likely to continue to rise for the next year or so, even if mortgage rates rise. Inventory cant just be created out of thin air.

+ 1

Powell just told us today that he will not be taking inflation seriously.

Wrong:

What he told today is that he still has his and others money in the market

Once the assets are removed you may see an increase in the rates but no real timetable on that removal.

Friday Market and Monday following may be interesting

The Weimar hyperinflation lasted as year and was over, if you really wanted to describe his doings, you’d call him Caracas Boy Powell.

Saw an article once that final year of hyperinflation means nothing in the big picture. Inflation robs the people of 95 – 99% of their wealth in the years leading up hyperinflation stage.

Went to Ace Hardware to buy some 1/2″ copper 90s and 45s, plus unions for an essential plumbing job-water leaking under house. Most of the bins empty, what remains, six to seven times the price a year ago. WTF!

Food too, hard to do numbers, but $40 for meat for a meal for two. Outrageous BidenFlation! People are getting really pissed off, like I never saw them before.

I wonder how much of this is due to hyper consolidation, in that the oligolopys are now playing games with how much they can increase prices until we cry uncle. It doesn’t matter what industry you look at – consumers are screwed. It’s not until there’s two or three players left in an industry that the FTC finally wakes up. Every city in the US used to have multiple local banks, for example. There were so many that they didn’t even bother naming them well. The first national bank of bumbletown, the second national bank of bumbletown, etc. But hey, the executives and shareholders all got wealthy, so that’s all that counts.

When will people realize that the economy is not a computer where you punch in a number and the answer pops up a fraction of a second later. It takes TIME for rate changes punched in to filter through to street level.

Want to blame someone for inflation? Go back to 2019 and the three rate cuts that still weren’t enough for the Pres. He wanted NEGATIVE rates. But lumber prices didn’t double the day after the third rate cut. Or the next month.

Biden is the one who has instructed the Fed to control inflation and the Fed will obey but it’s going to take TIME. Don’t blame new guy for former’s decisions.

Wish I could give you a medal for this!

Biden REappointed Jay Powell to the Fed. Kamala Harris rushed back to DC to cast the vote that prevented Judy Shelton, a progressive Fed Member’s appointment. That’s all I need to know.

Armbruster,

Shelton was sunk in the Senate in Nov 2020, when Republicans still had the majority, because several Republicans voted against her.

To advance the “time” hypothesis, it has taken a lot of time for our government under the leadership of Bush, Obama, and Trump to concoct what it is that we have now. Bail outs and QE galore. Agree on the negative rates comment, but the lumber prices, etc. that we have now is directly correlated and caused by severe changes in our economic system at the outset of COVID. Most would concede its utility in March/April 2020 when no one knew what loomed ahead, but come January 2022 and we’re all in commotion about it. Just because someone has employed sensible rhetoric about combatting inflation does not mean there is sensible action to back it up. We are well past the need to punch in a number to raise rates, like 10 years and counting. And not the gentle 25 bps increments being touted now or the momentary 2.25s in 18/19. The ruling class has been neglecting sound economics as a new American past time.

Tom,

Our local hardware store, several days ago, offered a galvanized 3/4″ cross-tee fitting for…$14.70, standard Tee was well over $7.00…each.

FWIW

I have a U.S. customer with 13 truckloads sitting in Vancouver, B.C. for 3 weeks now and could only book 1 to ship this week.

Biden and Trudeau have sown the wind.

Are the bond vigilantes finally returning? 10 year closes highest in two years at 1.867%.

Wolf, something you might want to do an article on – monthly chart of BND says the bond market just put in a lower-low to match the lower-high last summer. Arguably this signals the first bond bear market in 4 decades, started back in mid-2020. (I suppose I could put an article together too, starting to gain confidence after Sunday…)

For the past 40 years, no one in the US has faced the prospect of simultaneous bear markets in both stocks and bonds. Bonds are mostly safer than stocks, but today neither is a genuine safe haven, particularly with inflation on the loose.

The total bond market index fund, BND, rolled over in mid-2020. On several technical metrics BND hasn’t been this weak since 1994 (or before). However, back in 1994-95 BND was only down for one sharp spurt, it didn’t put in fresh lows a year later. But that’s what BND just did this month.

And now, perhaps, the stock market has given way also.

Reminder: the bond market is much larger than the stock market. Also, changes in the bond market affect the cost of all future loans, including rollovers of existing debt – not just prices of current bonds. So even though Mr. Bond’s price swings are smaller, it’s economic impact is really large. This is perhaps why the US, EU and Japanese central banks have avoided raising rates in any meaningful long-term way for 4 decades.

But today, inflation leaves no choice. Until the production economy gets retuned and goods become abundant again, inflation will drive interest rates higher, and drive other policy choices as well. Hopefully some will be less dumb than telling people they can’t work, can’t raise prices or can’t sell in the middle of a production crisis. The market needs the right signals to restore routine production.

Wisdom Seeker – Thank you!

This is true for bond traders. But not many retail investors are bond traders because it’s hard to do, and because liquidity of specific bonds is low and you cannot trade those bonds, and because you get screwed by your broker if you try to trade them.

But people who bought bonds at issuance — and the bonds don’t default — and who hold to maturity will get face value. So maybe yields on that bond are shitty for 20 years, but ok, they get their money back, plus the coupon payments for 20 years.

The issue is bond funds, and people who own bond funds. These people don’t get face value of the bonds. When there is a run on the fund, the fund can collapse, and people lose 60% or 70% or more in a fund they thought was holding investment grade bonds, while investors who hold the same bonds outright will get all their money back at maturity, and will collect interest along the way.

Even when there is no run, but just lots of redemptions, the fund sells its bonds at lower prices, and fund holders will only get part of their money back, while holders of the actual bonds will get all of their money back, plus coupon interest.

I hate bond funds, as you can tell. I’ve discussed this before.

Owning bonds outright is OK if you bought at issuance and hold till maturity. If you bought over the past few years, you just get a shitty yield for the duration.

And at that stage it becomes a finger in the wind, I guess for many.

Will I be able to offload these bonds I bought from podonk services to someone for a good price before anyone realises:

1) The price needs to be a hell of a lot lower before the yield approaches anything like real inflation (pick your measure, say anything from shadowstats)

2) This company primes the issuance I bought.

I’ve had bond funds over the years and have done OK in a falling interest rate environment. But if interest rates spike this will no longer be the case. I still have a short term muni bond fund which has very little yield, but very little fluctuation. Its an “old lady” investment if there ever was one. Junk Bond funds are the worst investment mankind has ever invented for the reasons you described above.

The risk of a run on the fund are not disclosed. When it happens, the fund collapses. This happened with big bond funds during the Financial Crisis, including a bunch of Schwab’s biggest funds, the Schwab Yield Plus series of funds, which was marketed to risk-averse investors. They lost 60% to 70%.

To get a feel for the law suits that came out of it, Google schwab bond fund class action

He cant cant spoil the midterms.

Inflation spoils midterms.

What if he secretly hates Dems?

I’m sure he does. Don’t most people? 🙂

Yeah, leftist here and I hate them. All.

What if the Democrats are deliberately handing power back to the GOP because they don’t want to be blamed when bidenflation leads to a bidendepression?

I heard that Whitehouse was telling Powell to address inflation as it is number one concern for Americans now.

No, our number one concern now seems to be Ukraine; gotta stoke that up even though it really has nothing to do with us. Our cities are full of homeless people, military spending is somewhere close to a trillion dollars per year, our industrial base is hollowed out, public infrastructure has been allowed to rot, the 1% are getting away with murder as they accumulate billions upon billions. Life for many Americans now is 3rd world quality.

why do people keep saying this? the average joe doesn’t care about the stock market.

This is true before the FED turns the stock market into a GIANT casino. Last year, many of my in-laws started “investing” or really trading stocks for the first time ever. They brought cryptos, SPACs, worthless POS companies, etc., on Robinhood, Webull, and the likes. I can tell you, they care about the markets.

Over the course of 2021, I had different friends and family discuss getting into investing three times, each citing friends who “have been doing really well at day trading and investing in cryptos”

Those were a trigger for me to do a little selling and keep building up cash. Couldn’t help but think of the shoe shine boy story.

Average Joes actually care about the stock market. They know their bosses lay off when the stock crashes and hired when stocks soar. When stocks crash and inflation is high- average Joes clip coupons and pick every penny off the floor. Most of the time Average Joes are working school nights to help feed their family and end up falling asleep in economics 101. Most teachers felt for the Average Joe and signed him up for DECA classes. This is where you go to school for a 1/2 day and work a part time job 1/2 a day. They do not get the education needed to understand the stock market. However, they do care. It hurts them more then you can imagine!

I think the cost of housing over rides that at this point. They don’t care if it crashes if it means eventually shelter costs decease.

I mean, I live in hillbilly country and even they are talking about it.

The Average Joe doesn’t care but the average-by-dollar-volume Democrat (or Republican, for that matter) political campaign DONOR certainly cares.

And one suspects the average primary voter cares more than Average Joe too.

Until at least midsummer, the election isn’t a battle for Average Joe voters it’s a battle for donors and primaries.

“Sen. Elizabeth Warren (D-Mass.) on Monday said Federal Reserve Chairman Jerome Powell’s failure to disclose requested information on the trading scandal that rocked the central bank suggests that the Fed is hiding the full scope of the situation.

Warren penned a letter to Powell on Monday reiterating her request for the Fed to release all available information regarding trades made by central bank officials in addition to the ethics changes the bank announced in response to the trading scandal.

The Massachusetts Democrat noted that she previously sent requests for information on Oct. 21 and Dec. 7, both of which were not answered. She is now requesting that details be provided by Jan. 17.

She said the officials’ failure to provide information “raises suspicions” that the Fed is not publicly disclosing the full extent of the trading scandal.

“I am deeply concerned that your continued refusal to release information about Fed officials’ trading is at odds with your stated commitment to address the scandal ‘forthrightly and transparently’ and that, particularly in light of the new report, it raises suspicions that the Fed may be failing to disclose the full scope of the scandal to the public,” Warren wrote.

A Fed spokesperson told The Hill that the central bank has received the letter but does not have any further comment.”

Still nothing but crickets on this.

The Fed and its cronies banksters along with congress have laughed at Warren for years. These folks have increased their wealth many times over since she began office. There will probably be a few retirements with full benefits if anything.

Why would Fraudsters aka FED would give into requests. Unless they are looking at prison term they won’t relent.

We all know she is a straight arrow. Get it.

That woman is all talk, all the time.

Then why not find a Judge, in a Court of Law, to issue a demand for the FED to release the information? They can refuse her; but not the Judge. So why not?

This administration has the opportunity to shape the future of this country right now, but they don’t have the balls. What they should do is send the FBI in to arrest Powell and all the other central bankers who were front running the markets, and announce it on live tv, showing the perp walks. Hang the entire inflation situation on the FED and their corruption, and announce sweeping new policies to combat systemic corruption. Unfortunately, the FBI itself is shot through with it.

How about “Sen. Elizabeth Warren” and the FBI get a copy of Powells Personal Phone numbers and hand it to CNN .

Right now, the corruption is throughout most of the system. (I thought it hilarious that so many Americans thought that any of the billionaires would fight the corruption that enabled them to amass their fortunes.) The judges and the politicians should be investigated, because an amazing number of them become millionaires or billionaires and as to lower court judges, they usually have assets that cannot be explained by their puny salaries.

The only way to weed out corruption is complete transparency: they should be required to make public what assets they have on the day they take the bench or get to their positions and what assets they have in total each year and how the assets increased. I think that they will claim amazingly good luck in always choosing the best investments, so that their assets balloon after they take office.

That is why I am not troubled by the congressperson’s insider trading: I prefer that type of corruption (which is open and does not make them beholden to the ultra-rich or organized criminals) to them accepting bribes. Too many of those objecting to the congresspersons use of inside information to trade stocks are politicians owned by the ultra rich.

Also keep in mind that this administration does not have such an “opportunity” because it does not truly even control the US congress. Those, of both parties, who have clearly blocked raises on taxes on the ultra-rich, etc., are the ones truly in control.

I bet AIs could also be developed able to be truly effective polygraphs, except certain people who have some mental issues, like psychopathy, which can be detected by other means. I bet those congress persons will also vote against that funding, it if were proposed.

Let’s say you contract on a new home. You’re pre-approved. At a certain interest rate. Takes 6-9 months (being generous here) to build. Oops, sorry mister builder I can’t qualify at these new interest rates. Banks don’t lock in interest rates for 6 months.

A lot of people are in this situation. Some of my friends have booked new homes which would be delivered to them in 6 months plus.

Not true. A typical custom construction loan would run 1-2 years, depending on your house. Big houses take more time to build. Not uncommon to have options for cost overruns and time overruns.

Plus the interest rate is fixed when you sign the loan.

A custom construction loan is interest only during the period of construction, then rolls into a fixed rate loan.

I have done dozens of these.

The point is when can the fixed rate on the post-construction fixed rate loan be locked in?

Can it be locked in when construction begins or only much nearer to completion?

If the latter, mortgage rates might have shot up during the construction period – by 150bp or even more.

When you sign a custom construction loan the interest rate is normally locked in when you sign the loan [or it can be locked in 30 to 90 days prior to closing, depending on your bank, etc.]

The payments are interest only during construction.

At the end of construction the loan [typically] converts to a conventional 30 yr fixed loan at the agreed interest rate.

Banks really really don’t want to take back a custom house so the loan has to be very secure.

If you are good, some banks will let you be your own contractor. But you had better know what you are doing.

I haven’t done any since I retired 10 yrs ago. Things might have changed a little.

So the custom construction loan rate is locked at construction time BUT the “conventional 30 yr fixed loan at the agreed interest rate” at the end of construction is NOT – it is whatever the prevailing market rate is at that time which could be MUCH higher. So Gomp is right.

Custom construction loans, where you hire a general contractor to built the house, or owner built custom construction loans, are “off the books” so to say, with secondary lenders. They buy the loan after the house is finished. Then the original bank takes the money and loans it out on another construction project. They make money on loan fees and interest, so the bank wants the house finished and the loan sold asap.

But the construction lenders are almost unregulated and have a lot of freedom on what they loan for and who they loan to [as long as they can sell the loan later on].

So if you can convince a bank that you know what you are doing, you can start out investing in RE as a builder and save alot of money.

And have fun. Designing and building stuff is very satisfying.

“conventional 30 yr fixed loan at the agreed interest rate”

The loan IS locked into a 30 yr fixed when you sign the loan. It NEVER goes up.

You pay interest on your construction while you are building the house.

Say you have a building lot which you own free and clear.

Worth 400k. That is your down payment. The bank takes that as collateral for the loan. They loan you, say 800k to build the house. The bank does an appraisal based on your approved building plans. As long as the house appraises higher than 1.2 million you are good to go.

As you make progress on the house you get draws to pay the subcontractors evey month. When the house is finished it converts into a conventional 30 year loan [that can be sold].

If you sign a construction loan on Jan 1, with a 4% interest rate, and finished the house Dec 31, the interest rate for the next 29 years is 4%. It doesn’t matter if interest rates jump up to 10% while you are building. You are locked at 4% until you sell, or pay off the loan or choose to refinance.

[I left out a couple of unimportant steps.]

That is an option but only a small portion of the homes under construction are built as custom homes and financed in this manner with a construction loan by the homeowner. The major builders sign a purchase and sale contract with buyer and the closing isn’t until after completion and the buyer uses a typical loan that locks the rate in the last 60 days.

I locked a loan for 8 months earlier in January. I saw the writing on the wall and decided I needed to hedge. Bank offered 3.25 + .5%. (cost of rate lock) total 3.75 and $1,000 non refundable fee for locking (goes towards closing costs if I sign with the bank). I figured if in 7 months the rate is worse than 3.75 I win, and if it’s better they let me float down ONCE or I can walk and lose $1,000. I’m pretty happy with my decision right now, only wish I had locked when it was 3.0 the week before.

Does anyone know WTF this gold/lumber index doom flasher means? In my neck of the woods my back hoe, track hoe, flat bed and sheet rock haulers traffic economic metric is way down. All the box store building supplies isles are loooooooded with high priced materials. OSB board stack is so high it’s damn scary to walk by. Sheds in the back are looooaded. I asked the lumber manager will the prices be slashed to move it. He said he was too busy watching his stock go up to give a shit. I’m rich bitch. For context, He knows me as a regular pest that asks a lot of questions and that bitches about the lack of quality Oak 3/4 in plywood for cabinet carcasses I build. I also bitch to him about not getting rid of damaged sheets from the stack. I know where he hides out back in the Contractor area and I track him down.

“I know where he hides out back in the Contractor area and I track him down.”

Good Job!

Has to be a buyer’s strike or a buyer and producer strike both. I live in a lumber producing area and am seeing far fewer trucks with finished doug fir 2×4’s and 2×6’s on the highway.

Based on what they do, and not what they say, the Fed’s dual mandate is to support stonks and housing. They’ve certainly failed on stable prices, while employment is so distorted/jacked-up with stimulus, it’s hard to say what’s going on there. This stonk and housing bubble (aka the everything bubble) has been accomplished to a large degree by unprecedented and extraordinary QE. QE is buying US Treasuries (debt monetization) and MBS (driving mortgage rates down). Mission accomplished. However, the following relationship still applies:

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” – Milton Friedman, (1912-2006) Nobel Prize-winning economist, economic advisor to President Ronald Reagan, “ultimate guru of the free-market system”, A Monetary History of the United States 1867-1960 (1963)

So we get massive inflation in assets first and then in general prices. It’s almost as if Joe Biden is channeling Jimmy Carter or something. 🙂

The Fed is still “doing” QE; they haven’t started tightening yet and won’t until sometime after March, when QE tapering (reduction in purchases, but still going strong) is supposed to end. And then, somehow, the Fed is claiming that they’ll initiate QT, when they actually start reducing their “balance” sheet, which is still growing and now essentially at $9T. Good luck with that. BTW, the Fed’s balance sheet is BS. A real balance sheet has assets and liabilities, while the Fed’s is all liabilities, purchased with ex nihilo, or out of thin air $. It’s magic!

All of these extreme machinations are complicating everything, but they’re only postponing the inevitable adjustment to the financial system and real economy. We may even get actual price discovery at some point. A centrally-planned, command-and-control financial/economic system is always doomed to fail. Think Gosplan and the (former) USSR.

In my view, we’re still living in housing bubble 2.0, which is merely an extension of the same policies as housing bubble 1.0, and we all know how well that worked out last time. Three serial bubbles in 20-odd years, brought to you by the Three Stooges of the serial arsonists at the Fed. Interesting times indeed.

Summary: All asset markets are jacked-up by the Fed’s monetary and Washington’s fiscal policies. The Fed should have raised rates and stopped QE a long time ago. Can anyone say “policy error?” Unfortunately raising rates is going to kill the over-indebted economy and asset markets, so I think that’s why the Fed isn’t actually doing this. However, they’re only delaying the inevitable crash and making worse, since the peak keeps growing the longer they stimulate. Oh the humanity!

“There is no means of avoiding the final collapse of a boom brought about by credit (debt) expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit (debt) expansion, or later as a final and total catastrophe of the currency system involved.” – Ludwig von Mises

“Based on what they do, and not what they say, the Fed’s dual mandate is to support stonks and housing.”

The Fed certainly failed in your dual mandate today, with prices of stonks and bonds falling and yields spiking. The 30-year mortgage rate today hit 3.74% on the way to 4.0%. Up from 2.7% not long ago. That’s how you cool a housing market.

Wolf,

What do you make of this comment by Powell today?

“Roll over at auction all principal payments from the Federal Reserve’s holdings of Treasury securities and reinvest all principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in agency MBS.”

Looks like they want to keep buying MBS but stop Treasuries when QE ends in March?

DM,

All of QE will end in “early March.”

After QE ends in early March, to keep balances flat while Treasuries mature and MBS get reduced by passthrough principal payments, the Fed will have to buy enough securities of both types to replace those that roll off.

What we learned today is they will shed ALL their MBS over time and reduce the balance of Treasury securities.

https://wolfstreet.com/2022/01/26/yields-spike-stocks-dump-futures-fall-asia-sags-after-powell-explains-how-the-fed-will-crack-down-on-inflation

Thanks for that perspective here. I certainly welcome higher mortgage rates, and I would welcome even more a return to a free market system without the Fed and their endless machinations, interventions, and financial repressions. Waiting for the ghost of Paul Volcker. Not holding breath.

The dual mandate I’m referring to is based on Bernanke’s Thu., Nov. 4, 2010 Wa Po Op Ed where he extols the virtues of the “wealth effect” in stonks and housing:

“Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

Again, I welcome any rational policy that returns us to more sane markets, including an r* ex financial repression. However after easy $ for 13 years now since the GFC, and all of the associated distortions that come with it, I don’t see a “soft landing” scenario. Bubbles always burst. In this case, due to a highly indebted (global) economy, I don’t see rates rising much, since crash ensues. I would love to be proven wrong on higher rates BTW. I also think that the Fed’s policy on inflation is to encourage it in order to inflate away a significant portion of the large steaming pile of debt.

Bernanke’s philosophy is absurd.

Inflating asset markets doesn’t make a society wealthier. It’s equivalent to “printing”, other than the beneficiaries differ.

Any of us individually is wealthier (on paper) if asset prices increase but this doesn’t translate to the entire economy because there is no increased production or supply.

It’s a belief in something for nothing, complete foolishness. It’s irrelevant if someone with a PHD believes or claims it. It’s still a lie.

In a non-distorted economy, lower rates are evidence of a more prosperous economy. But since lower rates are mostly or entirely artificial since at least 2008, it’s actually a negative sum game, after accounting for the economic impact of malinvestments.

There comes a point when the large steaming pile of debt hits the fan.

Impossible to inflate it away.

‘It’s almost as if Joe Biden is channeling Jimmy Carter or something.’

A slug in the history salad. When your folks took you for an ice cream, did you keep saying ‘are we there yet?’ It’s common ground even among economists that it takes a year+ for interest rate changes to reach Main Street as distinct from Wall Street. The stew we’re choking on today was not cooked yesterday.

Which Pres virtually ordered the Fed to lower rates? Which Pres has told the Fed to control inflation?

> The stew we’re choking on today was not cooked yesterday.

Man, ain’t that the truth. It took 4 Presidents, 4 Fed chairs, and a whole chain of complicit Congresses to get to this point. Granted, Biden served in various capacities during this time but the people who think it’s all Biden… smh. GHWB got skewered for the economy in ’92, but you could also argue that he set up the 90s boom for Clinton by cutting on needless defense spending.

If the Democrats were actually smart, they would have tanked the 2020 election and hung this whole thing around Trump and the GOP’s necks. But their thinking is even more short term than the average American’s.

SSDD!

Semper Fi

Rollercoaster ride on a broken track. Powell does what they tell him to do, period. They have to keep pumping liquidity or the entire system implodes like a building demolition. Any chimp knows these facts by now.

Construction cost : the move from 2009 low to 2013 high is equal

to the move from 2020 low to the current high. It’s probably over.

All other charts are below their highs.

Michael Engel,

I’m not 100% sure I understand what you’re trying to say. But just in case, here is the construction cost index, as an index, which shows the cumulative nature of those cost increases. Doesn’t look like anything is “over” just yet (the black dot is June 2020 when the spike began):

I work in warehouse development and can tell you hard costs are up ~35% from 18 months ago and that hard costs are continuing to increase at 2-3% PER MONTH right now, with no sign of abating. Most general contractors won’t even sign guaranteed maximum price contracts because the subcontractors won’t commit to a price.

Not to mention the timeframes needed to pre order steel and other materials so you can get it built on some reasonable schedule. The extended timeframes are another additional cost to all construction projects.

Wolf,

Dig up a graph from the Ford/Carter’s era of 1973 to 1978 and I think you’ll see the same pattern. That’s when the Nixon/Connally wage price controls were taken off and construction costs went through the roof. Interest rates followed. Prices could only go so high and then we had an energy crisis and recession in 1980/1981. I think we’re repeating the same pattern once again.

Wtf?!

Now what? Is Powell letting rates rise with bond holders selling? Is he getting the market to hike the rates for him? Sitting this one out from here.

1. Never start a fight against a government guy or mole. He knows everything and suspects nothing. He dont know what he is sayin…

2. Inflation will be easily tamed by the hint of future rise in rates. Execept its not. Because I went to the stores, still the prices are high in every retail supermarket.

3. Stocks may raise or fall. Nothing goes in a straight line. Obviously. we know.

4. Gasoline prices are still high. In the swamp area around $3.22 average in the cheapest places who accept only cash.

5. If there is a lag time to see the price reduction in the supermarket, house prices will reduce in 2-4 years of time.

6. I hope Fed will not raise rates above 0.25% otherwise, I have to buy the mug from wolfstreet.

even if the prices remain at current level in the future it means inflation as fallen to zero.

Rates 7% below inflation…

I’m going finance my mug.

I bought my mug 6 months ago. Must have doubled or tripled in value by now.

Maybe we need a Wolf Street Mug CPI?

I never have taken delivery because I’m a skilled futures trader.

Caveman

I saw one on Ebay advertized for $350. Hell, I’ve got an extra one. I’m thinking of putting it up for sale. I’m gonna ask $500 and see if I get any takers.

Friend filled up his tank and said “$70 dollars! And this tank is smaller than my previous truck”. I chuckled. Then I got gas for my compact SUV and it too was $70 bucks. That hurts. 13 gallon tank so the math is Cali Gas at $5~

WFH helps a lot

Well at least nat gas has stayed flat even though oil ran from 65 to 75.

At least we can still heat our house cheaply during the winters

Silver has not risen in price too. There are some commodities people do not want

My old S class has a big tank and takes 91octane and takes about $80 if empty.

My scooter runs 87 and takes about $2.75.

More WTF ripples from COVID, overlaid unfortunately on a drunken punchbowl of previous Fed excesses. But like Bernanke in 2008, having arrived here, from here, what else could they do? Print, or face apocalypse. Uncle Jerome was still leaving plenty of wiggle room in his calming lullabies today. As he must. Problem is, a lot of alternatives have been missed, narrowing the path. Hopefully all players sort of muddle forward not too crazily, and it all sort of cobbles along. Hoping the big unforeseen shocks just stay away for awhile. Yeah, sure.

Cost of standard extruded red clay brick (non-cored) still remains the same for the past 30 years.

8″x2″x4″ brick at Lowe’s is 54¢ as of today.

It is even cheaper by the pallet.

1000sq ft starter house requires approximately 40,000 bricks.

House with solid brick walls ( not plastered with bricks ! ) will beat crappy $1M shack made of 2″x4″ and wrapped in Tyvek hands down.

Because the lifespan of that crappy $1M shack should not exceed the duration of 30 year mortgage.

Planned obsolescence I might say.

The only problem is – country is not teeming with good bricklayers after Ivy League quietly abandoned PhD program in “Masonry and Bricklaying Science”.

I disagree. I like brick and have used it in quite a few houses as an accent.

But in the Pacific Northwest we have strong building codes and inspections.

A new house here has extensive engineering and quite a lot of steel strapping tying all that wood framing together.

A structural engineer I worked told me many years ago “Houses fall apart and then fall down.” House plans now have to be stamped by a certified structural engineer.

All that strapping and tie downs keep the house together during earthquakes or big wind storms.

Long time ago I worked as a bricklayer.Our bricklaying crew -2 helpers & 4 bricklayers – usually finished 1000sq ft house in 10 days-after that electricians,carpenters,plumbers and plasterers took over.

Standard pallet was (and still is) 534 bricks,each bricklayer laid 2 pallets during 10 hour shift.

Yes,we put wire mesh inside brickwork according to building code,no big deal,did not take long…

What pissed off my coworkers big time was that I used mason’s lead,6′ long pieces of L-shaped aluminium attached to the corners and built picture-perfect house fronts with 0 tolerances.

Meanwhile my coworkers ,old farts mainly,were dragging feet and marked time,measured and positioned every f… brick with a level etc…

Eventually somebody stole my leads and I migrated to greener pastures.

But I still admire good 200-300 y.o. brickwork.Maybe somebody now admires house fronts which I built too 😁

Hi Brent .

Could you give a more detailed explanation of the bricklaying technique you used please.

Thanks.

fred gassit

@Fred

Look up Youtube video “Marking the gauge for laying bricks”

Even while using makeshift devices – gauge rod and clamps – this guy builds perfectly straight wall 1/2 brick thick.

I used factory-made L-shaped aluminium gauge rod with holes.

This device mightily increases output & quality but alienates your fellow crew members to no end 😁

I’m in a stick- built house built in 1928 that is fine. Previously owned a 1948, also fine. Had it re-roofed, sheathing was tongue and groove planks. So little damage to it repairs were no charge. Around here if yr sheathing is OSB it MUST be replaced to reroof per regs. Not safe to walk on. The main problem with modern stick- built is OSB. It’s a time bomb and should be out of the Code at least for roofs.

BTW: oldest continually inhabited buildings in the world are wooden. In Japan. OK they aren’t plywood, but a stick- build with ply, with a roof kept up, will last longer than exposed reinforced- concrete.

Air-dried lumber with unextracted resin will last forever,like log houses in Henry Ford Greenfield Village.Because resin is natural protection from insects and mold.

Now they quickly kiln-dry lumber,extract the resin and treat lumber with formaldehyde.

In 2009 I saw new developments demolished for lack of buyers.Tyvek sheets flapping in the wind & 2″x4″ covered with black spots of mold.

Brent:

Please review ALL the findings from the results of the 1989 Loma Prieta earthquake from the downtown Santa Cruz, CA area…

Especially with re: ”brick” construction; some from early days, approx. 1850,,, some from much more recently.

Otherwise, consider that almost everywhere in many decades, ”brick” has been a ”finish” outside of either reinforced concrete or reinforced ”block”,,, or even outside of wood frame in many places.,.

You may also want to consider/study the actual results of testing of brick with and without all the modern structural steel additives,, e.g. ”horizontal ladder” reinforcing at every third layer, etc., etc….

VNV

LA Times and SF Chronicle cover Cali earthquakes big & small pretty well.I read about Loma Prieta.Also I read that Cali in 1981 passed the law about reinforcing all solid brick buildings.Slowest progress is in San-Bernardino due to permanent holes in local budget.

The good thing is – not all areas are earthquake-prone like Cali.All of them are well-known thanks to tectonic plates theory.

And we,the unlucky non-Cali dwellers,can still build solid brick houses and inhabit them worry free.

Our crew put wire mesh between every 5 layers of brick, with wire ends sticking out, so the building inspector may check code compliance.

I think that if you put wire mesh between every layer of bricks this house will survive 1MT nuclear blast.

Now-please google:

San Francisco Landmark #271

Bourdette Building

90 Second Street,SF

Solid brick walls,built in 1904,was completely undamaged by the Great SF Earthquake of 1906.

Is not it something we all shall imitate and even try to surpass ?

I just watched Powell taking questions after the January meeting. Clearly, the current inflation rate is acceptable for him. Additionally, he has no expectation that inflation will accelerate, or become entrenched.

Also he stated that the Fed will never target an inflation rate below 2%, and that their goal was to establish -an expectation- that inflation will be 2% on average.

I also watched Krugman. Now both of these clearly just find inflation on the high side but acceptable. There is no rush.

Powell also emphasised that the main tool will be the funds rate, not QT. So treasuries are going to run off at a snails pace. He stated that he expects some fiscal damping whether Biden’s on board with that who knows.

I got the feeling that their view of, basically of not being able to anticipate the current 7% rate of inflation was that certain things were unexpected i.e. the great resignation, supply side, but this seems to be regarded as well we were a bit off but no biggy.

There were no questions about housing, stocks or the reverse repo facility. There was also a point when in reply Powell said “thats what it says” so presumably they are taking their cues from their model produces (which is entirely fair of course).

IMO inflation can spiral higher from the emergent sentiment of the US consumer but thats not what the Fed data is -currently- showing. Plus there is no shock and awe policy in the wings, he’s well maybe 25 points up maybe not.

“Clearly, the current inflation rate is acceptable for him.”

Hahahahaha. Keep being denial. It’s good for your soul.

https://wolfstreet.com/2022/01/26/yields-spike-stocks-dump-futures-fall-asia-sags-after-powell-explains-how-the-fed-will-crack-down-on-inflation

Regarding the second chart: “New Houses By Stage of Construction,” the red line, “New houses under construction,” peaked at 340K in 2006 or thereabouts. The green line, “Completed,” lagged and topped out just below 200K. That’s a difference of 140K. Did the 140K homes that were under construction never get completed?

Prophet,

The second chart is inventory by stage of construction. Once a house sells, it comes out of inventory. There were a lot of sales at all three stages of construction.

About two thirds down is the section “Sales of New Houses, in Total and by Stage of Construction.” This tells you the sales of houses by stage of construction. This is what came out of inventory.

From bls.gov:

How seasonally adjusted data are calculated:

There are several programs and variations that can be used to construct a seasonally adjusted series. A common program used at BLS, is X-12-ARIMA, developed by the U.S. Census Bureau.

Wolf, do you know if these figures include; ??

1. modular homes

2. mobile homes

3. kit homes

or any alternative owner built homes such as hay bale and earth construction??

These are single-family houses built by homebuilders.

There is a separate data series for manufactured housing, which is what you’re talking about. I don’t cover that.

Thanks. I’m now wondering if new mobiles and alternative builds on land are taking more of the market share.

It’s fairly common where I am for people to live in unpermitted shells and other weird structures on their own owned land.

OK, mobile home deliveries only went up a bit for the last 5 years.

Wolf,

This was really interesting! Up here in Canada we have incredible low inventories, and a central banker that still claims its transitory with the foot on the gas. But inventory buildup in everything is getting me worried, that perhaps the loose policy will be the arson requiring the central bank to be the firefighter again.

The reason I believed for the low inventory was speculation and investors which have doubled down in this easy money environment up here. From this though, I wonder how much is because the new supply of houses has slowed due to construction delays. A new home owner only sells their existing home, when then new is finished. Selling before you actually get the new house is rather risky with delays.

This build up of inventories of partially complete and stuck in transit, chips, appliances, construction material, houses, if relived, could suddenly flood the market and we could swing from under supply to oversupply of inventories. I was speaking with the local hardware store guy, and he was telling me they had orders from first half of last year that not yet arrived, and some 3 or more back orders for some goods. He was not worried if they all arrived, since they could send what they did not need back to head office.

What would happen to inventories if you returned the under construction and to mean and added it to completed?

One dollar, one vote. If my dollars have been made worth so little, then so are my votes.

Everyone should vote out All incumbents on election day.

We’re doing a new renovated condo in the Trinadad Neighborhood of DC. A few years back this neighborhood was so dangerous that the police had to put roadblocks on several streets to prevent entry for everyone except those who lived there. It is still a drug infested neighborhood with a lot of vagrants hanging on the streets. But it is coming back with investors and new homeowners, including families with young children moving in. The condo sold at fair market value without any problem. The condo market is alive and well in the Swamp. Not like what is happening in other parts of the metro area and in other cities.

The FED doesn’t let rates rise or make them fall. The fed FOLLOWS markets …. ALWAYS. Once you understand this basic premise, everything is much simpler and all the conspiracy theories become just that.

Yes, the fed WILL raise rates now because the free market already raised its rates by over 1.0% in the last year and a half. Will the fed jump immediately by 1%. No. they’ve already showed us their hand. They’ll catch up slowly, at the same time hoping free market rates (and inflation) start to moderate and come down gradually.

The worst of COVID is already over (except in the press). Prices SHOULD start to normalize at higher levels than pre-covid, but not keep blowing out to the upside. Car prices are already coming down. If prices DO keep going up, demand will drop and we’ll have a nice big recession and …. interest rates will drop again too, as in every recession.

The bond market is actually way bigger than the fed, especially when you consider treasuries, corporates, foreign governments and corprates

CCCB,

“The FED doesn’t let rates rise or make them fall. The fed FOLLOWS markets”

This theory is idiotic BS, promoted by people who are clueless about how the Fed operates.

One of the Fed’s fundamental operating procedures is that the Fed tells the market what it is going to do MONTHS ahead of time. With this Fed (not the Fed from 50 years ago), there are no surprises.

To communicate what it will do, the Fed uses the “dot plot,” speeches by Fed governors, Powell’s testimony before Congress, the FOMC minutes, etc. That’s why I discuss those things in my articles, so that YOU know months ahead of time what the Fed will do.

This is the official operating procedure of the Fed. In bits and pieces, the Fed outlines what it will do months ahead of time.

By mid-December, we knew the Fed would hike by 25 basis points in March. This was widely communicated. And I wrote about it at the time. Just because you didn’t read it, doesn’t mean it doesn’t exist.

By mid-January, Powell confirmed the date of the rate hike: March 16. Two months ahead of time.

Today the 3-month yield is still only 0.2%, within the target range of the current federal funds rate (0.0% to 0.25%) but moving up slowly. The Fed will move its target on March 16 to a range between 0.25% and 0.5%. We know that because the Fed told us so, but the 3-month yield will take the next six weeks to get there.

Short-term yields will gradually approach the raised target range. And when the Fed officially makes the announcement on March 16, everyone has already priced all this in because the Fed has told the world what it will do, and then it did it.

On paper, some fools who refuse to see how the Fed operates assume that because the 3-month yield started rising two months ahead of the rate hike, that the Fed follows the 3-month yield.

But this theory is BS for the consumption of the braindead. The market follows what the Fed says in the prior months. You’re just not paying attention, and you’re not reading may articles that are telling you months ahead of time what the Fed will do.

CCCB, I have a troll here who keeps promoting this BS. And I just delete it — after having wasted my time shooting down this BS five times in a row.

I didn’t delete your comment this time but instead explained what is going on. It seems you have never read a single thing that I wrote about the Fed, or else you would have known better. I cannot believe that this BS is still circulating. It’s just like a zombie, it’s dead but refuses to die.

Comments are closed.

The Fed’s big liabilities: reserves, US paper dollars, RRPs, and the US government checking account. Reserves already plunged by $1.03 trillion.

Interesting stuff happening in the labor market, suddenly.

It sticks to plan, QT like clockwork: What the Fed did in details & charts, and my super-geek extra-fun dive into the “To Be Announced” market for MBS.

Huge losses, but now revenue growth is slowing. Hilariously, executives refer to the huge losses as “profitability.”

“Temporary” inflation is suddenly runaway inflation. But the negative-interest rate idiocy and QE are finally over.

Copyright © 2011 – 2022 Wolf Street Corp. All Rights Reserved. See our Privacy Policy

Powerful Wealth Building Resources