THE WOLF STREET REPORT

Imploded Stocks

Brick & Mortar

California Daydreamin’

Canada

Cars & Trucks

Commercial Property

Companies & Markets

Consumers

Credit Bubble

Energy

Europe’s Dilemmas

Federal Reserve

Housing Bubble 2

Inflation & Devaluation

Jobs

Trade

Transportation

Home sales that closed in August were made somewhere from a few days to a couple of months before they closed – so roughly around and before the peak of the summer bear-market rally in mortgage rates and stocks that started in mid-June and ended in mid-August.

By mid-June, the average 30-year fixed rate mortgage was at or above 6%, having doubled in less than a year. And stocks had sunk. But then the tightening-deniers fanned out and trolled the media with nonsense about the Fed being “dovish,” that it would “pivot” in September or whatever, and they declared that inflation was “over,” etc. etc., and stocks bounced off their mid-June lows and mortgage rates fell from 6% to 5%, and for a moment just below 5%. And Realtors were already talking about how the housing market was picking up again.

Now we know that all this was a hoax. Mortgage rates are now solidly over 6%. Fed chair Powell finally got through to everyone with his Jackson Hole speech that the Fed will tighten further. Inflation got worse and has shifted to services, from where it’s difficult to dislodge. And the stock market, now finally seeing inflation and higher rates, has given up most of the bear-market rally gains.

But back then, it seemed real enough to lots of people. In the San Francisco Bay Area and in Southern California – whose housing markets are heavily dependent on the stock market – there were hopes of an uptick amid re-surging stock prices, plunging mortgage rates, and gorgeously imagined Fed pivots. Those were the Good Times. So here is what we got instead from the California Association of Realtors for August:

Prices sank further. In four of the five big Bay Area counties, prices were down year-over-year. Sales volume was dismal, though slightly less dismal than the collapse in July. Time on the market about doubled year-over-year. And supply surged year-over-year.

Sales volume, single-family houses (SFH): -24% year-over-year, slightly less dismal than -26% in July.

Median time on the market: 20 days, up from 15 days in July, and up from 11 days a year ago.

Supply of unsold inventory: 2.2 months, same as in July, compared to 1.7 months a year ago.

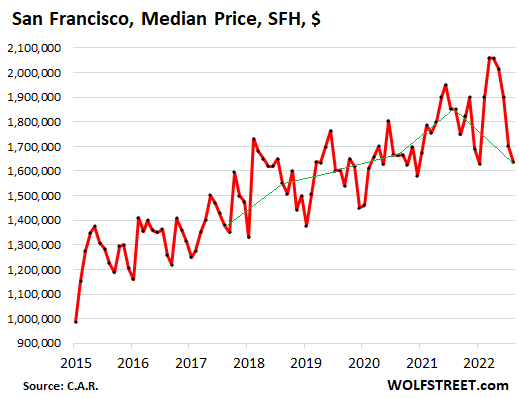

Median Price, single-family houses: $1.635 million, lowest price for any August since 2019 ($1.60 million): -3.8% from July, fifth month in a row of declines, -20.6% from peak in March, -11.6% year-over-year.

In San Francisco, prices usually hit their seasonal lows in January or February; so this will be interesting. The green line connects the Augusts:

These are massive price declines in San Francisco. Yes, median prices are volatile, and we look at them with a good dose of circumspection, and trends need to be confirmed over time. But this trend here is being confirmed nicely so far.

One glance at the chart tells us that the median price will eventually bounce again, to zigzag lower rather than to go to heck in a straight line.

Sales volume, single-family houses: -28% year-over-year, less dismal than -46% in July.

Median time on the market: 16 days, up from 14 days in July, and up from 8 days a year ago.

Supply of unsold inventory: 2.0 months, compared to 2.6 months in July, and 1.4 months a year ago.

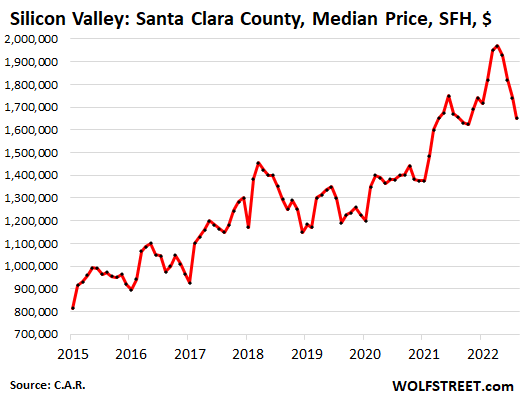

Median Price, single-family houses, $1.65 million: -5.2% from July, fourth month in a row of declines, -15.4% from peak in April, -0.3% year-over-year:

Sales volume, single-family houses: -30% year-over-year, slightly less dismal than -35% in July.

Median time on the market: 14 days, up from 12 days in July, and up from 9 days a year ago.

Supply of unsold inventory: 2.3 months, compared to 2.2 months in July, and 1.5 months a year ago.

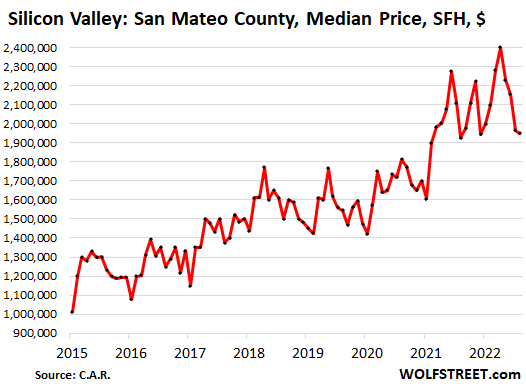

Median Price, single-family houses, $1.95 million: -0.8% from July, fourth month in a row of declines, -14.5% from peak in April, +1.3% year-over-year:

Sales volume, single-family houses: -30% year-over-year, less dismal than -35% in July.

Median time on the market: 16 days, up from 13 days in July, and up from 9 days a year ago.

Supply of unsold inventory: 2.1 months, compared to 2.4 months in July, and 1.3 months a year ago.

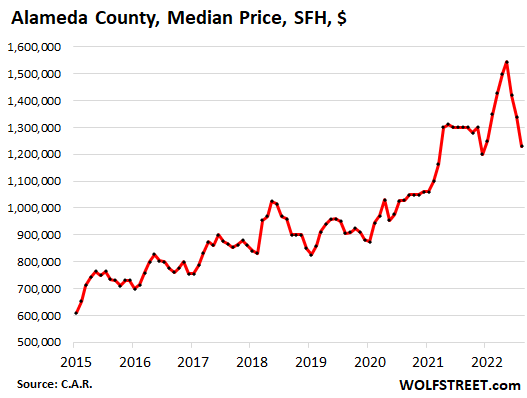

Median Price, single-family houses, $1.23 million: -8.2% from July, third month in a row of declines, -14% from peak in May, -5.4% year-over-year:

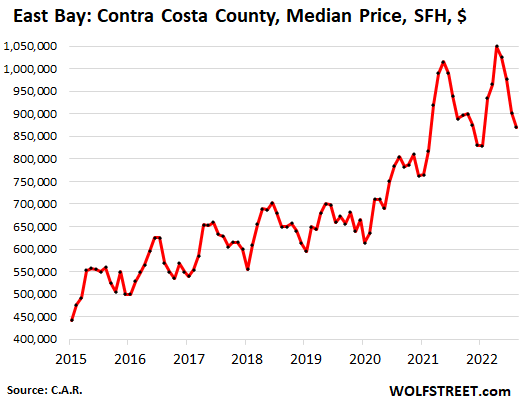

Sales volume, single-family houses: -27% year-over-year, less dismal than -36% in July.

Median time on the market: 18 days, up from 13 days in July, and more than double the 9 days a year ago.

Supply of unsold inventory: 2.3 months, compared to 2.5 months in July, and 1.4 months a year ago.

Median Price, single-family houses, $870,000: -3.6% from July, fourth month in a row of declines, -10% from peak in April, -2.2% year-over-year:

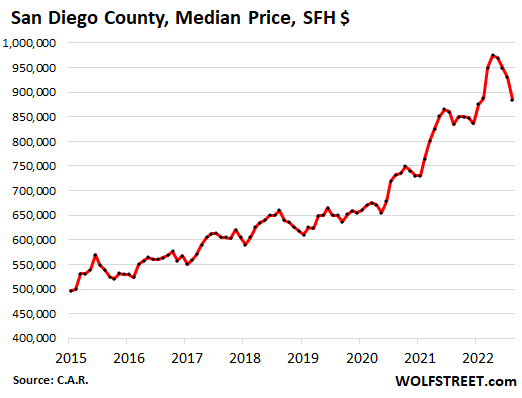

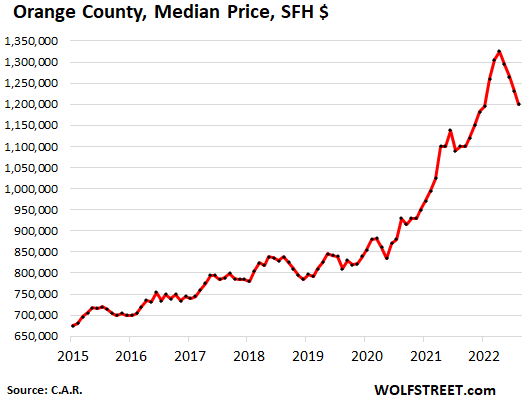

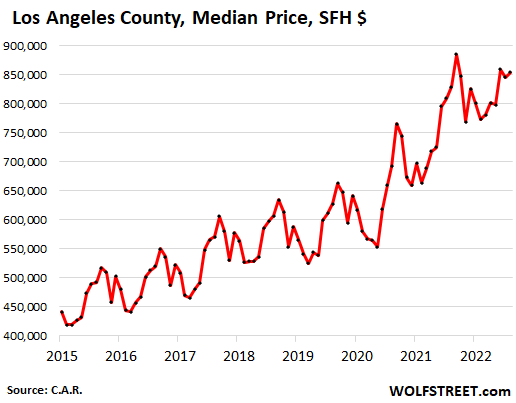

In Southern California overall, house prices fell for the third month in a row, -5.9% from the peak, which whittled the year-over-year gain down to 4.6%. So here are the three biggest counties. In San Diego, the median price dropped nearly 5% from July. In Orange, it dropped 2.5%, but it ticked up in Los Angeles. So here we go, starting with the most splendid housing bubble, San Diego.

Sales volume of single-family houses: -28% year-over-year, less dismal than -41% in July.

Median time on the market: 15 days, up from 10 days in July, and nearly double the 8 days a year ago.

Supply of unsold inventory: 2.5 months, compared to 3.1 months in July, and 1.7 months a year ago.

Median Price, single-family houses, $885,000: -4.8% from July, fourth month in a row of declines, -9% from peak in April, which cut the year-over-year gain to +6.0%:

Sales volume of single-family houses: -30% year-over-year, less dismal than -39% in July.

Median time on the market: 17.5 days, up from 13 days in July, more than double the 8 days a year ago.

Supply of unsold inventory: 2.5 months, compared to 3.0 months in July, and 1.6 months a year ago.

Median Price, single-family houses, $1.2 million: -2.5% from July, fourth month in a row of declines, -9% from peak in April, which cut the year-over-year gain to +9.1%:

Sales volume of single-family houses: -29% year-over-year, slightly less dismal than -32% in July.

Median time on the market: 16 days, up from 13 days in July, nearly double the 9 days a year ago.

Supply of unsold inventory: 3.1 months, compared to 3.3 months in July, and 2.0 months a year ago.

Median Price, single-family houses, $855,000: +1.0% from July, -3.5% from peak last September, +3.0% year-over-year:

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.![]()

Email to a friend

For the first time in a long time… would love to see California export some of that price-dropping love across the country.

More importantly…

Will this stop the equity locusts from California from infecting other more sane lands with both their pricing out the locals and voting patterns.

One man’s sanity is another man’s dementia. Each to his own.

I think the people leaving are more of the conservative persuasion.

I always recommend Tulsa, OK. Beautiful place, no earthquakes, except those caused by the fracking industry with their injections wells, and it’s nice and warm there in the summer. And at least you don’t get hurricanes. And you’ll get used to the tornadoes. Housing is super cheap. Politics and politicians are always perfect in Oklahoma. And Tulsa still pays people $10,000 to move there if you bring your job with you. I lived there for a long time. Plus, life expectancy (74.1 years) is 5 years less than in California (79.0 years), which is great because it saves a lot of money and hassles later on in life, I guess.

Wolf, I think some people missed the sarc. LOL

Mr Richter, I love your site, its always a learning experience. While I’m all good with sarcasm and consider myself fairly thick skinned, but admittedly dense. This isnt the first time you imply that a person who would leave a beautiful sunny CA. $1.2M 3/2 in to reside in a 240K Tulsa 3/2 are, idk, somehow less than because what, weather? culture?? political belief??? Im just not sure what you mean but would appreciate clairification. But if Im just a “less than” in the opinion of someone I respected Ill just move on.

nefff,

If all you’re looking for is cheap housing in a decent-size city — if cheap housing is your #1 priority, and living in a decent size city, is #2 — Tulsa is hard to beat. I always tell people, rent a house or an apartment for half a year, and see how Tulsa suits you. And then you decide.

That is all cable media/real estate agents myth, Florida grew only grew by 1.1% last year, and Texas grew by 1.2%. Better than the US growth rates, but still pitifully low for “boom” states. Interestingly, Delaware outgrew both states (not sure why). Only Idaho is growing decently (2.9%) but from a really low base. And the silver tsunami starts next year (boomers start exiting the market is mass – i.e. starting dieing in mass). Florida real estate is going to be spectacularly bad for 10 years. Florida is huge leaky bucket problem.

A mass die off in boomers?

Next year?

So like a Logan’s Run or something?

Gotta a couple more years of Florida living until I can escape.

I’m actually zeroing in on Tulsa for the reasons Wolf listed. Plus Oklahoma has the most progressive medical cannabis program. I’m a patient.

Delaware has no sales tax, the property taxes are low, and the cost of housing downstate is cheap compared to where most people come from. Many retirees from New Jersey & Eastern Pennsylvania move there for the lower cost of living, but still quite close to any family left behind. Source: lived there for 10 years; was surrounded by Jerseyites in my community.

No way bud.

I’m 4th generation. Half the damn country came here.

1 year treasury crossed 4%. Probably better choice than a bank CD. Let’s see if mortgages cross 7%.

Edit: let me be first to put this out there. It will come out (sooner or later) that Elon Mask was manipulating the options market. You just watch.

You saw the insane gamma squeeze in the options market too? Musk is a conman without match IMO.

RE prices are going back to a minimum of pre plandemic levels. Since things always overshoot, I would not be surprised to see prices up to 25% below that

When S&P/Nasdaq went down 4% for a day, VIX was like 27-ish (lowest ever was such s move).

Up about a double on Appl, Msft, Amzn, and few other puts.

Tesla refuses to budge. $300 is like a magnet. Someone bought 38,000 Jan 300 calls ($140 Mil) all in one swoop 3 days ago. Daily dollar volume on Tesla is like Apple+Msft. It will tank all at once, fingers crossed.

I believe the whole move up last week was because the big wall street firms had done estimates and knew the cpi would disappoint and tank the market so they ran it up before then to compensate. I’m short a mortgage company that was starting to tank and out of nowhere last week the stock recovered and then day after day this week barely budged a penny. On top of that some sleazy bucket firm came out with a buy rec, target price a mere 5% or so above it’s current level. Lol, such fraud.

Historically stock market ,could deflate another 50-60% .Housing prices could lose 70% ,when there’s no fuel to heat them .

Fed had no exit strategy when they went to zirp and QE. There was always going to be be pain in assets and in real economy when experimental policy ended. Real wages and real investment income getting punched in the nose with more to come.

We are in the midst of mark down of the price and the real earnings of stocks and rental real estate. Bag holders going to be fooled again. Hope I was smart enough not to be one, but not so sure til we hit bottom.

You mean MMT doesn’t work? What?

Even Jim Cramer is buying treasuries now.

Apparently he told his investment club that he is buying 2-year treasuries.

He stated that on cnbc ,ladder your treasuries in3 month 1 year, and 2 year treasuries more secure .This is best advice a pro can give pathetic

Concerning the spread between median time on market and supply, can someone give some color to why there is such a large spread? Does that mean there is a huge inventory of high/over priced homes that are not selling? At face value, the numbers seem contradictory. Thanks in advance.

Wolf’s explained it like this:

Buyers are on strike due to high rates which destroyed affordability.*

Sellers are in shock and denial, unbelieving that their beautiful shack won’t sell for as much as it used to.

So there’s a gulf between “bid” and “ask” with few on either side having the courage to bridge the spread.

*The bear market in stocks isn’t helping buyers either. Stock and option cashouts are a major portion of down-payment and/or cash-payment money in Bubblefornia…

How does that square with the fact thst once you list a home, it sells in 16 days (when there is 5x that number of homes in supply)? Are you agreeing that the only way those two numbers can square up with each other is that the overpriced homes have slowly been accumulating on the MLS over time? Don’t most people get around that by removing their property from the MLS for a week, then relisting? I still don’t see a definitive answer. Is there data out there related to this question?

JeffD, I am not sure I understand the conflict you are seeing. The supply has to do with the rate at which people are listing houses compared to the rate at which people are buying them. Keep in mind that median means that half are below the number and half are above. If there is a surge in new inventory (with 0 days on the market), the supply would go up and the median time on the market would go down. If those houses don’t sell, the median time on market would start to increase. Also note that as you point out houses are usually delisted after a while (sellers usually have a 90 day contract with a broker) so there is a cap to how high the median time on market can go.

I agree there should always be a positive ratio between the two. The large 5x ratio is what I am having trouble wrapping my head around. Look at the data for San Diego above. The supply is going down, not up, which I am having trouble relating to one of your arguments. I’m not saying the numbers are wrong, I just can’t wrap my head around the relationship. I need an example, probably described over time, to understand how such a large ratio can come about. Unfortunately, I’m beginning to believe the size of that explananation may be beyond the scope of the comment section. Perhaps this might be a good reference article to have as a permanent resource for the site? It’s ok. I’ll just muddle through.

JeffD, I think it’s pretty simple actually. Houses are much less affordable now to the average buyer because of interest rates on 30 year mortgages having doubled in only 6-7 months. But sellers are not willing to sell for significantly less than they could have sold their houses for only a year ago. So they either are not listing them, figuring they’ll wait until the Fed pivots and interest rates drop (sending prices up again) or they are listing them at the old prices. The latter group is why supply is up significantly.

That said, most buyers are not willing to pay the prices that were set when interest rates were 3% when interest rates are now 6%. So the most saleable houses (those that have just been renovated, are in a desirable location, are priced slightly less than the others, etc.) are still selling relatively quickly. HOWEVER, there is only a small pool of buyers willing to pay current prices, as everyone else, as I described above, realizes that prices should not be as high as they are given current rates.

So the houses that the aforementioned small pool of buyers aren’t interested in sit. My guess is the other listings don’t get much interest, and the sellers remove them from the market.

Realtors play all types of games to coax someone to pay more for something then it is actually worth, driving up all the prices and in turn driving up their personal commissions; it’s their job to do it, that is why someone hires them, it’s a giant Ponzi scheme, a game-but games are not part of the economy so in the long run all of the real estate none sense that is going on today will smooth out. Trying to figure out something stochastically is a waste of time because there is a constant, high, probability that you are still wrong in your calculations; you cannot afford enough data to be accurate. And I really have to agree with you that there is some type of game like relisting the home or just simply marking the home contingent whilst whispering something sweet into the home sellers ear_ Some type of game that the general public or some little guy like me has not figured out as of yet…..

To be clear, I’m expecting a 2 to 3 sigma standard deviation, but given the data values, I feel like the standard deviation given the relation between these values is much, much larger. Again, I don’t think the numbers are wrong, I just don’t see how to arive at a “resonable” standard deviation given something like a poisson probability distribution, which I might expect for home sales. (My real problem may be that I don’t understand what probability distribution best maps to home sales).

My problem might be that the median time on market is an exponential distribution, while the supply is a poisson distribution (both poisson processes), but still, not getting it.

It’s simple actually. There’s always a lag between actual pricing and price discovery. The two have to align over time. When you have outliers that can screw up the numbers, that doesn’t help. The ultra rich who buy multi million $ homes don’t care what the market is, and will buy at asking or close to it, so those multi million $ prices screw up the mean if not eliminated. I’d say that you probably have quite a few of those on the West Coast. You could see how a few of those sales would weigh heavier that a larger number of $20,000 price drop on a $220,000 home.

Standard deviation is meaningless when a market changes from bullish to bearish etc. they are qualitatively different regimes in a nonlinear dynamical system.

I interpret this snippet concerning the Central Limit Theorem differently:

“their properly normalized sum tends toward a normal distribution even if the original variables themselves are not normally distributed.”

Since real estate data is an aggregate, there is no “out” as I see it. I don’t think there is a required Equilibrium assumption, like there is (for a continuum) in the engineering discipline of Statics.

Wolf, as this goes forward and the trend is seen throughout the nation it might be interesting to note where housing sees the least decline in median price. Wherever is the least correlated with the stock market sounds like a great place to me.

I will bet my shirt that the Boston metro will see the smallest variation. There is just not enough land to build and the NIMBYs are solidly entrenched.

People in San Diego think the same.

We are special and this time is different and everyone wants to here.

Personally for me.. one can’t even pay me to live in Boston. Its just me.

I heard some in Cali are subleasing their basement out to make ends meet on their mortgages, and the worst part of all, what will they have to talk about at parties when everybody used to talk about how much their house was going up?

California homes have basements? I have never seen one!

Basements in some areas, yes. No, you don’t need them at all, but the people who built them were “refugees” from cold, northern climates who brought their zip code with them. It’s part of their ethnic identity.

Some of these houses also have “canning kitchens” because the mother was *required* to can all the family’s food: you just couldn’t trust what “they” (commercial packers) put in those “boughten” cans! Not to mention steeply pitched, snow load roofs, multiple fireplaces, raised wood foundation, small windows, etc.

I could tell stories! They were my in-laws, the Germans from Russia aka “North Dakota Germans”. They are still around and you can read up on their culture via internet.

“North Dakota Germans” — my great-grand-mother. She was one mean old lady.

Years ago I looked into building a house in Arizona and coming from the East Coast I wanted a basement. I was told that the cost of adding a second floor was much cheaper than the cost of excavating a basement. In the East Coast they have basements since the foundation has to be below the frost line which is several feet deep so you might as well use the space.

Correct. The frost line is around six feet down if I remember correctly, so if you’re going to excavate six feet, you might as well do two more and have a full eight foot high ceiling basement.

Einhal:

Not to pick the fly stuff out of the pepper, but the frost line in most areas of the northern states is 3 feet (for example in IL). Four feet in the waaay cold areas.

Basements, as such, do not exist in coastal California due to liquefaction of the soil. The water tables are high in many areas and, when the ground shakes, it has the potential to turn to mush. The “basements” might be lower levels in homes built into hillsides.

Delisting houses to impact the days on market is not a new phenomena. It is quite common, especially in areas where there is a high incidence of second homes. The peeps put them on the market and, if they don’t sell during “the season”, yank them off and they go into a category known as “pocket listings” where a realtor knows it’s for sale and, if they get a prospective buyer, can gain permission to show the home. Those “pocket listings” do not appear on the MLS.

Lastly, house prices fall in reverse order of the way they increase. What that means is that the last homes to rise in price during bubbles (those with incorrectable defects such as a freeway in their backyard, adjacent to a shopping center, located on a busy street, etc.) are the first to fall when things go south. The well maintained homes on an interior parcel in the same tract are usually the last to fall.

There are no basements in California. Check your source.

false, retired ca. gen. contractor.

while not a full basement perse, many, especiallly older homes at least in the L.A. area 2 story built before 1950 have basement/ 3rd level below grade areas w/ furnace/water heater + storage areas that could easily be converted to a couple of small bed rooms, I worked on plenty of houses and apartments with this set up…

People are renting their bedrooms and garages for decades

The quality of life has life has gone down the drain big time.

Yeah, but the Fed destroyed interest rates/printed money for 20 years so the sociopathic used car salesmen/elected officials of DC could ignore America’s fundamental economic problems for 2 decades.

And that is what really matters, isn’t it?

Still over a decade of fed policy baked into these 2015-x charts… no pain yet, just minor annoyance…

Exactly.

What were median sales prices back the last time when mortgages were over 6 pct (the 90’s)?

Since median income growth since then has been pretty crappy (broken up by long periods of *really* crappy) then affordability translates into late 90’s median home prices or sales volumes collapsing by 70 pct plus.

The ZIRP “rich” can hold their breath and not sell, but they will have to hold it for years and years unless the Fed caves.

Do major metros in Cali also have a very high multi homeowner rate? I’ve not been able to find a stat with Google, I think here in Metro Vancouver where I live we are around 20% if I remember correctly. I can see a potential of RE getting absolutely crushed with rising interest and all the leverage in our markets. Rents are skyrocketing so maybe landlords are able to offset the increased borrowing costs but I’m not sure how long that can work, young workers were already cramming into apartments prior to increases so not sure how many more can fit into those units with wages not keeping pace.

LA County not looking too bad, for the time being. There’s very limited inventory in coastal markets, which contributes to the drop in volume.

Nationwide, for sale inventory is about 8/13ths of pre pandemic normal.

Only the inventory normalizes, prices will collapse.

Just saw the below statement on MSN main page.

The Fed should raise the Fed Funds rate from 2.5% currently to at least 3.5% this month, not the expected 3.25%. Then the rate steady for remainder of this year if the inflation rate at least drops to 6%.

That means ignoring pleas from billionaires and others who are overly concerned about the stock market being about 19.5% below its 52-week high.

———————————————————————-

” The U.S. economy is teetering on the brink of a serious downturn if the Federal Reserve doesn’t pump the brakes on its rate hikes, billionaire CEO Barry Sternlicht said. “

Maybe if billionaires paid taxes we wouldn’t be in this mess ,only w2 ways out of this mess .Flat rad everyone pays ,or default.

How does tax get changed to rad

It’s not possible to tax fake wealth at scale because it isn’t real. That’s the “wealth” of most billionaires, from an asset mania. Any attempt to do that would send asset prices crashing and the cost of anything bought with it soaring because production doesn’t exist to accommodate it.

Can’t argue with those stats but the sales volume needs some perspective. Single family homes are barely being built here anymore, moslty multi family now and for the foreseeable future. That’s a huge contributor. I have a bad feeling about what’s coming soon, though. As much as I’ve been bullish on San Diego, I’m worried that a macro event is going to teach us all a hard lesson.

Sure, few new SFH are being built in the city of San Diego. But this is the County of San Diego. And besides, all this data is “existing homes,” sold by one homeowner to the next, not “new homes.”

And since you mentioned them, condos…

Condo sales in San Diego: -31% yoy

Median condo price: -6.5% from peak in May

I don’t have the full data set on condos or else I would post a chart.

The county is not producing SFR’s anywhere near the levels it did in decades past. The city has policies that are destructive to the existing inventory of SFR’s through a massive expansion of the state’s adu law. The single family home, the one we all knew as kids with the swing in the tree, a garage, small garden, etc. is becoming much rarer here.

Condos are gonna get kicked in the butt big time. There are way too many of them being built, also multi family rentals. The rate of declining appreciation of this market will be way more than SFR’s.

Im not questioning that things are gonna slow in appreciation or even start to drop, just saying that there are really strange forces at play here, specifically the city, but also the county, especially with regards to there being virtually no land available for the massive tracts of the past.

My friends are still buying sfr in San Diego.

Their reasoning is.. condo prices may fall but not sfrs as sfrs are not being built anymore:-)

Agreed. I think the only substantial sfr tracts we even hear about anymore are on the outskirts, north of Escondido, south east Chula Vista, misc smaller ones in the east county, etc. No more rancho this that and the other being built off the 15. Stuff is still being built off the 56 but not many folks could’ve afforded that even when rates were 3%.

The days of starter home Mira Mesa type developments are long gone in San Diego.

Combine this with the fact that so many homes are being bought here by the work from home crowd who still find this place to be a deal as compared to the Bay Area, as well as those coming in from other parts of the country. San Diego isn’t only selling to San Diegans. Nationwide affluential income demos are a large part of the market here.

The working class wanting a starter home will be either driving north to the inland empire, going south to TJ, or going quite a bit into the east county.

This is standard and has been for decades: if you want a newly built house with a yard in a big city, you need to go move to the burbs and deal with urban sprawl. That has been the tradeoff for years as cities become denser. I have no idea why you keep bringing this up. That’s how it is everywhere. Don’t complain that they’re not building new SFH in city centers. If you want a newly built SFH with a yard, move into urban sprawl. That’s what urban sprawl is for.

I heard this that every one wants to live in San Diego.

Let’s see. During last downturn even super limited and expensive areas life Lajolla went down 40 percent or so.

I’m not sure I made my point well enough. Within the county there’s hardly any new single family being built and what’s in the city is being taken up. 7% of college area sfr homes, mainly 92115, have already been built out with second units.

Urban sprawl is no longer sprawl within the county, but folks are being pushed to other counties, specifically riverside county if they want a new home. It has been going on for years, correct, but it’s much much worse now. Just pointing out what I’m seeing here, I’ll leave it alone for now.

No, they’re NOT “being pushed.” They choose to because that’s what they’re looking for, given their priorities. If they want to live in a condo, or in a rental apartment, including big high-end units, there are plenty of them in great, more or less central locations. “…folks are being pushed to other counties” is like saying that people who want to live in a high rise in rural areas are “being pushed” into city centers.

People cross county lines ALL THE TIME to commute to work or to find a bigger or cheaper place to live. That’s not a biggie.

“You Can’t Always Get What You Want” — remember the song? It’s a fact of life, and most people have no trouble dealing with it. They compromise and choose, based on their priorities. Newly built big house with yard, go out to urban sprawl. Great central location, go to multi-family. What’s the problem?

And I still have no idea why you’re lamenting all this on an article about price drops in San Diego among existing single-family houses. There are lots of existing single-family houses in San Diego – even if few new ones being built. This wasn’t about new houses, but existing houses. And now prices are dropping. You should be jubilating, no?

Replying to wolf about op lamenting about lack of sfrs in sd.

May be he has affinity for high home prices for sfrs hence he thinks sfrs prices can’t drop in sd.

East country…like Yuma.

Where it isn’t so much a sunshine tax as a sunstroke tax…

Pretty much Arrakis, without the giant worms (so far).

1) San Mateo : waiting for a $3M check for fourteen days instead of twelve is not that bad.

2) MSFT was rising between 2013 and 2021, so is silicon valley RE.

3) There are many old folks in San Mateo who bought their house/houses

in the seventies eighties and during the dot.com boom. They don’t care about the a one year trading range.

3) MSFT was in a trading range for a decade between 2002 and 2013.

4) Zero rates allow buybacks, bonuses and executive perks. That’s how SF

political hacks fed themselves.

5) The stock market might rise, despite Fed hikes, if Nankie lose

the house.

6) Service inflation is difficult to dislodge. Inflation accumulation will

deflate San Mateo RE in real terms even without recession.

“1) San Mateo : waiting for a $3M check for fourteen days instead of twelve is not that bad.”

Wait… what this really means is that houses that didn’t sell got pulled off the market on average after 14 days in August, instead of after 12 days in July, and instead of after 9 days a year ago. I’m not totally sarcastic either — that’s an important metric: how long sellers are willing to leave their home on the market before they pull it. That shows how willing they may be to bend on price.

When a home doesn’t sell because the price isn’t right, sellers have some options, including: reduce the price until it sells (and many are now doing that) or pull it and relist later at a lower price.

In Bubble 1.0, some peak CA buyers had to wait 6 years to “get their price” (as in breakeven).

And that is assuming DC can endlessly rerun it’s ZIRP/money print scam.

1. Going forward, lot of younger people will never be able to buy houses or even retire in the old age. You own nothing and will be happy. So, don’t even bother.

2. West coast and LA-SD housing market is way different from the rest of the country. Even our famed “Arnold Schwarzenegger”, got his money from the real estate business. This is even before his acting career.

3. The GDP of California is so big even bigger than European countries. LA county has more population than the states like ND, SD, WY, MT, ID…

4. Are there any real data about the vacant properties in the west coast? because, even with really dense population, I would not be surprised to see empty houses.

5. Most of the houses are now similar to growth stocks. They simply grow in value, not for making revenues by rent, changes hands based on the value and always have a buyer.

6. Insane houses with insane prices during our times.

The only reason for California housing prices is a quarter century asset and credit mania, which includes foreign buyers. It’s as simple as that. Since we’re talking about most of an entire state (where most of the population actually lives) being abnormally overpriced, it isn’t because the place is so great.

The end of the credit cycle in 2020 and end of the (NASDAQ) stock market mania will be enough to end the California housing bubble, even as housing presumably remains noticeably more expensive than the rest of the country.

If California eliminated Proposition 13, a lot of the distortion you just pointed out would tail off. For readers outside California, Prop 13 is a law that says property taxes can’t go up more than 2% a year. My wife just sold her mom’s $1.5 million house that had a property tax of $1000/yr. If every Californian had to reset to property taxes based on assesed value, it would be the end of the world.

Give it time…those CALPERs pension shortfalls won’t pay themselves.

Some future version of Gov Hairgel will be talking up the “historical inequities” of Prop 13 (but pay no attention to that income tax behind the curtain)

The disparity between median home values and median household incomes in some of these CA areas is mind boggling. As expensive as RE has gotten in New England, deals are still to be had across the interior, particularly away from the major cities. Within a 45 min drive from Boston, household incomes average 120k+ with median home values in the 500-600k range. Meanwhile, 120k median household income (2020 census) in San Fran with a median single family house going for 1.635 mil. Future of big city CA homeownership will be ageing boomers and foreign investors.

Situation in Cali is completely unsustainable, which is why there have been such big declines in the past. Just look at case shiller plots. The recent run-up is driven by insane monetary policy. Unless that returns, housing here will decline significantly.

I’d hardly call $500K to $600K any kind of a deal and this is from someone who considers the area generally nice. It’s still a 4X to 5X multiple which isn’t affordable either except with artificially low rates.

30 YR fixed @6% is still artificially low, given the actual credit risk.

“The disparity between median home values and median household incomes in some of these CA areas is mind boggling.”

The median vs median comparison can be (and is) misleading. If everyone had to move and re-buy every year, a full mark-to-market, then it would be meaningful. But we don’t. It’s entirely possible that those actually buying have WAY WAY more income than the incomes of the legacy folks who represent the median.

Consider a ‘hood where everyone earns $30k. The median sale price is $1m mil. Thats crazeballs. But if those buyers have incomes of $500k, totally different story. Only a small portion of homes in any area sell in a given year, anywhere, so this is surely a big effect.

Median home value 14x median *household* income (pre tax) in main CA metros.

Last week, I saw a lots of news releases about white collar layoffs, hiring freezes, etc. that are happening at good companies on the West Coast. I think this is going to put an end to the housing price standoff we’ve seen the past few months. Once people are forced to move because of layoffs, housing prices will start dropping significantly. It might take 6-12 months, but I believe it is going to happen.

Layoffs not showing up as unemployment claims. Ppl are getting rehired fast.

So long as the labor market stays this tight, it drives further inflation – so the Fed will have to keep squeezing.

Houses’ prices are particularly difficult to judge. They seem to rise and fall according to the whims of the winds. The reason a house in a neighborhood seems to have a steep price is often social: the place has a good reputation and strangers want to throw in their lot there. We live in a world of strangers, and the catastrophic results strangers bring.

This time it was just for one reason:: availability of cheap money.

The retirement of baby boomers, who will sell their houses for money to live versus the purchase of US real estate by foreigners are two critical factors affecting California prices.

I am not surprised to many posts here claiming why Southern California is different and this time is different thus no major price draw down for housing in Southern California.

After all housing is religion here.

Only time would tell.

They’re pathological. Everyone who has lived there and left just laughs at their delusional psychosis. So many great places elsewhere in the country and world but they like their horse blinders apparently.

Its cultural.. I have found people in other places in America don’t mind trying to live in new places. But California has a different culture that it is comfortable with, particularly in So Cal. More ethnic diversity, etc. Food. Its hard to find places that are similar. New York, Seattle, Chicago maybe and those places come with a host of problems. Boston is not a food city. And the weather in those other places suck compared to LA or SF or SD.

Hence, many who were raised in So Cal cannot leave. Many who live elsewhere want to come here. I know people who have amazing careers in Boston want to leave So Cal to come to SF because of weather and culture. But that was when the economy was good.

Given the current economy, tech is going to eat losses, WFH will end since layoffs tend to happen to the outsider in competitive environments so people will come in to build relationships, if housing continues to decline, which it will, it will be an avalanche of homes being sold and california prices will reset lower. With interest rates having to climb, the zombie economy will finally end and the real economy will shrug off the fat, and the market will go with it. World recession. Housing will fall.

People will shed their standard of living expenses first, their stocks, their crypto. The last thing people will shed is their house, but it will happen. I wish there were another way, but the debt of this country has outstripped production capability.

Fed/government and Banks have run of out of their money and other people’s money and only choices are to boost production capability, or tighten the belt, or print money. Printing caused inflation due to demand outstripping supply and loss of trust, and the inflation ruins production capability development so tightening the belt (federal reserve interest rates) is the only choice. Housing prices will fall.

Food sucks in Boston? I guess you’ve never been to the North End.

compared to LA and SF and NY… Boston has good food here and there, but its variety is weak. Sure, some restaurants are amazing but its not the foodie city LA or SF or NY is… with a wide variety of good ethnic foods with lots of competition. just my opinion.

And i’m expecting home prices to fall in all of those places too. Second home locations/ future retirement locations will be sacrificed to save the primary home (although mortgage rates were so low, maybe not unless layoffs happen). I know people in Boston who bought homes in California so that when they retire they can live in SoCal or Bay Area. Its these homes that need to be sold to drop prices even lower. But these areas will always be more expensive than say Kansas City so its really more trying to figure out what price the real value is…

I agree with your forecast. In most cases all assets will be sacrificed to keep the primary residence.

Funny you don’t dare mention the specific problem those other cities face, but we all know what it is and Oakland is a poster child for it. The tribe and their pets only know how to destroy.

What are you talking about? There’s what, ONE such denial comment above? And one sarcastic one, too. Maybe you’re just seeing what you want to see?

No denial here. I wouldn’t be the least bit surprised to see -50%.

I’ve actually seen the “Bring any reasonable offer” tag put on 3-month old MLS listings for the first time in forever here near Charleston, SC. Shocking!

I’m seeing lots of listing on the West Coast where sellers are starting their price at an aspirational level, then reducing by 5%-10% every two weeks in hopes of arriving at maximum market price. This approach makes sense when there are suckers on the buying side who act out of FOMO, but currently I’m not seeing the suckers bite like they normally would have just six months ago.

I’m also seeing lots of houses that went pending/contingent in May, June, July, but are now back on the market. Buyers are second guessing themselves and are now exhibiting FOBB (Fear Of Being Bagholder).

The housing market has clearly changed, and it appears there now is a wide gap between buyers and sellers that needs closing over the next six months. Potential sellers who wait until next Spring to act may see asking prices down 10-20%, or more.

1) After 49 weeks the DOW weekly lost it’s grip. For fun and entertainment only :

2) The DOW built a Lazer tilting up in 2021: July 14 to Sept 20

and to Nov 29 2021 lows. // a parallel from May 10 to Aug 16 highs.

3) On Apr 18 2022 the Dow lost it’s grip and plunged to June low. Options :

4) Option #1 : June Low isn’t good enough. More to come.

5) Option #2 : The Dow counteroffensive will surprise the bearish traders. The Dow is pumping muscles to reach the Lazer at 37,000, a new all time high. Greedy/ fearful investors will fight each other …

6) We don’t know what will happen next !

7) A falling triangle is pointy on all ends

8) Soup is notoriously hard to eat when you’re driving.

9) You could drive a hard bargain on a used house now

While it’s great that prices are falling, there is a red alarm event I’m seeing up here in Bend. The home I rent has a Zestimate that’s down almost 10% from peak, however, the rent Zestimate is surging. Up at least 10%.

There is a giant pending housing crisis coming to middle/upper middle class renters.

The rents are going up. That is the problem. Why – because it’s easy. The owners of the multi unit condominium do not feel the need to raise the rents. They are still enjoying their yachts in the Bahamas or wherever. But they know that everyone goes up and that’s good for them, “the rents are going up”. So they go. And that feeds the inflation and poverty. So here is the next thing – “The real estate market is going down”.

The housing market didn’t just catch a cold, it went into cardiac arrest and died. DOA.

I’ve seen numbers where the payment on a median priced home is up over 60% since the rate hikes. Imagine that – you’d have to qualify to pay over 60% more per month to buy the same house as what you would have last February.

Jerome Powell, at long last, took the housing speculators out back and executed them. And now he’s sawing off the limbs of sellers, no anesthetic. There are vast swaths of houses which are now completely unsaleable, because buyers can’t qualify even if they wanted to.

Kunal and Beardawg are going to be drinking Mad Dog 20/20 together behind the local homeless shelter. Smug was never a good look. Karma sure is.

Your email address will not be published.

The purpose of MBS purchases was to repress mortgage rates and inflate home prices. That process has already started to reverse.

Retail sales without gas stations jumped 0.8% in August from July. Inflation shifted away from goods (retailers) to services.

Long-term stagnation turns into sharp decline.

Rate hikes to keep up with the Fed would work. But the Bank of Japan still digs in its heels. Its balance sheet has shrunk for months though.

But for yield investors: Short-term Treasury yields near 4%. Six-month CD yields at 3.5%, if you shop around.

Copyright © 2011 – 2022 Wolf Street Corp. All Rights Reserved. See our Privacy Policy

Powerful Wealth Building Resources