THE WOLF STREET REPORT

Imploded Stocks

Brick & Mortar

California Daydreamin’

Canada

Cars & Trucks

Commercial Property

Companies & Markets

Consumers

Credit Bubble

Energy

Europe’s Dilemmas

Federal Reserve

Housing Bubble 2

Inflation & Devaluation

Jobs

Trade

Transportation

The latest entry in the long litany of mortgage-lender layoffs is Citibank, which let go some people in its mortgage unit. Well Fargo, JPMorgan Chase, and numerous other banks, along with the non-bank mortgage lenders, have laid off staff starting late last year.

The biggest mortgage lenders aren’t banks. They’re nonbanks: Rocket Companies (owns Quicken Loans), United Wholesale Mortgage (owns United Shore Financial), and LoanDepot have cut their staff by thousands of people. LoanDepot also exited its wholesale business. AI-powered mortgage lender startup Better.com became infamous when its CEO mass-fired people via Zoom, which was followed by more layoffs. Some mortgage lenders have filed for bankruptcy. Others have shut down.

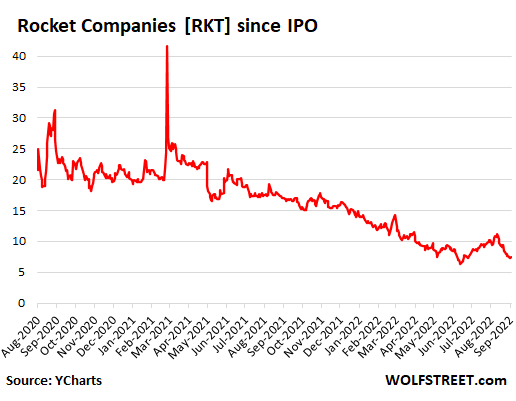

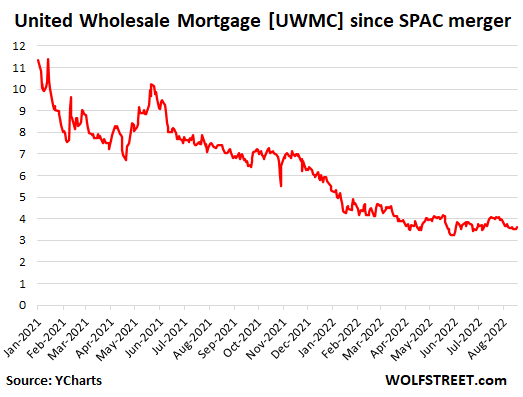

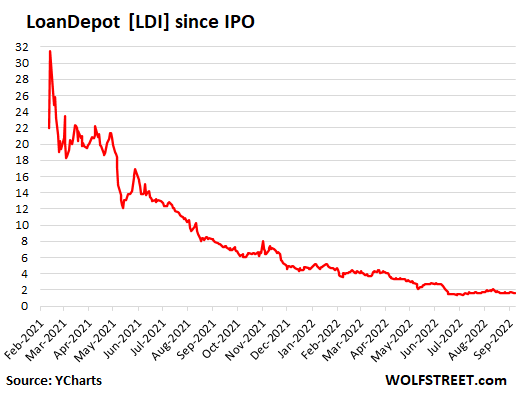

The stocks of the three biggest mortgage lenders have collapsed: Rocket Companies by 82%, United Wholesale Mortgage by 75%, and LoanDepot by 95%. All three went public either via IPO or via merger with a SPAC during the housing mania over the past two years amid immense hype and hoopla. All three have been inducted into my Imploded Stocks.

But mortgage lenders are not getting in trouble because homeowners are suddenly defaulting on their mortgages or whatever.

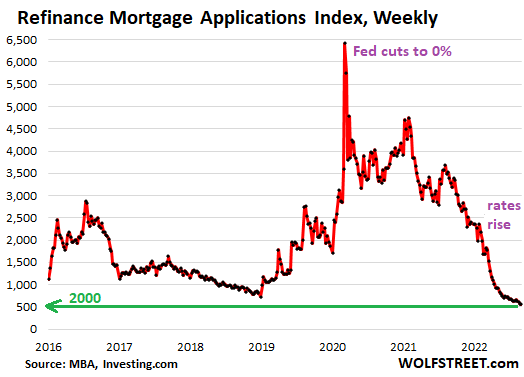

They’re getting in trouble because their revenues have collapsed because mortgage origination has collapsed, particularly refinance mortgages, where origination has collapsed to 22-year lows because few homeowners are going to refinance an old 3% mortgage with a new 6% mortgage, unless they have to in order to draw cash out, and that can be done more cheaply with a HELOC.

Applications for mortgages to refinance an existing mortgage fell by 1% in the latest week, having collapsed by 83% from a year ago, to the lowest level in 22 years, according to the Mortgage Bankers Association’s weekly Refinance Mortgage Applications Index, released today:

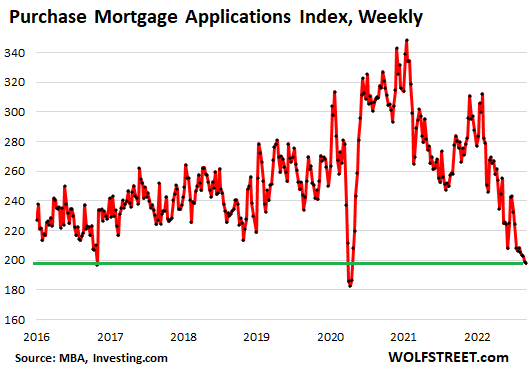

Applications for mortgages to purchase a home dropped by 3% in the latest week, as the newly returned 6% mortgage rates put a further damper on home purchasing activity. The MBA’s Mortgage Purchase Index has now plunged by 23% from a year ago and is approaching the lows during the April 2020 lockdowns:

The plunge in applications for purchase mortgages has for months shown up in home sales: Sales of new houses plunged by 30% year-over-year in July; and sales of existing homes plunged by 20%.

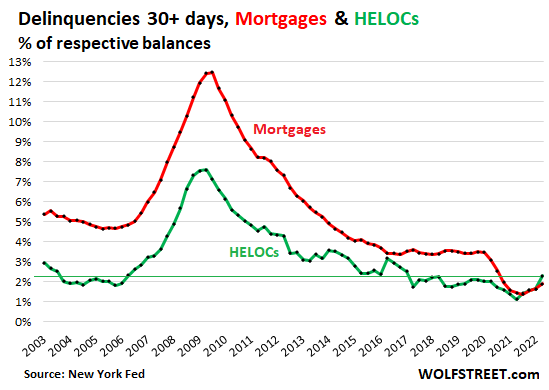

The mortgages that are outstanding have been holding up well. Delinquencies and foreclosures have started to tick up, but from the super record lows during the era of forbearance, when delinquent mortgages were moved into forbearance programs where homeowners didn’t have to make payments, and their mortgage was no longer considered delinquent.

The spike in home prices since spring 2020 allowed homeowners to exit forbearance in various ways, including by selling the home, paying off the mortgage, and walking away with extra cash. But the forbearance programs are being phased out.

So mortgage delinquencies have started their trip back to normal: Mortgage balances that were 30 days or more delinquent ticked up to 1.9% of total mortgage balances in Q2 but remain well below the lows of the Good Times (red line).

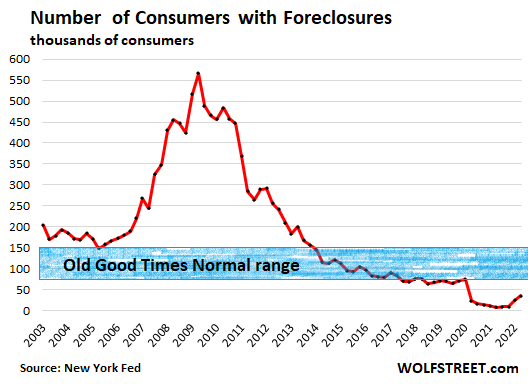

Foreclosures have also started to tick up but are still far below any of the prior lows before the pandemic:

The three largest mortgage lenders are nonbanks; they hold the mortgages they originate for only short periods of time, until they have enough mortgages together to sell them to Fannie Mae, Freddy Mac, the VA, Ginnie Mae, etc., which then securitize the mortgages and sell them to investors as MBS. These mortgage lenders, by not keeping mortgages on their balance sheet for long, slough off the credit risk to the buyers of their mortgages (and ultimately to taxpayers that guarantee many of these mortgages).

But during the period that mortgage lenders hold the mortgages, they’re exposed to the risk that mortgage rates spike, causing the value of the mortgage that has a lower interest rate to decline. This isn’t normally a big issue, but it was a big issue this spring when mortgage rates spiked by historic amounts in weeks, causing some losses among mortgage lenders.

These losses came just as revenues collapsed. Nonbank mortgage lenders get their revenues from net interest income (small portion of total revenues), gains on origination and sales of mortgages, origination income, servicing fees, etc.

At Rocket Companies, which surpassed Wells Fargo years ago as the largest mortgage lender – revenues collapsed by 48% in Q2, to $1.39 billion.

The company went public via IPO during the housing mania in August 2020 at $18 a share. Its shares [RKT] have collapsed by 82% from their high in March 2021, and by 59% from their IPO price, to $7.54 (data via YCharts):

United Wholesale Mortgage underwrites and provides closing documentation for mortgages originated by brokers, small banks, and credit unions. Its loan origination volume plunged by 51% in Q2 compared to a year ago.

It went public via merger with a SPAC. The merger closed in January 2021. The SPAC’s shares peaked after the announcement but before the merger closed, with an intraday high on December 28, 2020, of $14.38. From that high in December 2020, shares have collapsed by 75%. The chart only goes back to the date of the completion of the merger, to the first day the shares traded under their new ticker [UWMC]. From the closing high on that day, shares have plunged by 68%, to $3.61 (data via YCharts):

At LoanDepot, revenues in Q2 collapsed by 60% from a year ago, to $308 million, generating an astounding net loss of $223 million, compared to a net profit of $26 million in Q2 2021.

The company went public via IPO in February 2021 at $14 a share. During the first two days, shares performed a spectacular hype-and-hoopla “pop” intraday to $39.85, and then collapsed by 95% from that high, and by 88% from the IPO price, to $1.66 (data via YCharts):

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.![]()

Email to a friend

These folks made a lot of easy money when the policies of the federal government were driving house prices to the stratosphere, so I can’t feel too sorry for them when the situation reverses. As an aside, I wonder whether this crazy housing market would be a bit less crazy if the federal government exited the mortgage-guarantee business.

“Government is not the solution to our problem, government is the problem.”

Uttered over 41 years ago and still so true.

I read, probably here that the US backstops 75% of all residential first mortgages. No Moral hazard. The EU socialized health care, we socialized mortgages…

No going to happen. Looking at Wolf’s 30+ delinquencies chart, the point that mortgage forbearance returns will be somewhere in the 6-7% range. To get there, unemployment will have to move up close to Larry Summers’ recent 6% prediction. Will we actually get to that level of a recession? That’s hard to say. But, I don’t see it happening over the next 12 months. With the right black swan event; however, we could see unemployment approaching 6% by late 2023.

Most swans are white. Draught, flooding and war may crash the market for food internationally. With national debt payment crash shortly after as countries either choose to buy food instead of servicing debt. Or stop servicing debt after social unrest have thrown them into chaos.

Large flooding, wildfires, technical breakdowns and the like in a country is no black swan either. They happen ever now and then.

I am shocked to see gambling has been going on in this establishment!

A different flavor of 2008, a much more classic housing slump. I can hardly wait.

Meanwhile, draw down your HELOC while the funds are still available….

Credit crunch on deck for next year starting for all B credit companies and people.

A rated people (800 plus) will still have access to more expensive money.

When you can get a 5 year CD from your local bank, normalized finance will be delivered by the Fed.

So many comments have desired a return to tighter money, now buckle up.

Oh yeah, C rated foreign markets will splatter. Dollar denominated debt? Toxic waste….

We are all subprime now!

Be careful what you wish for. That toxic dollar denominated foreign debt could easily blow up the entire world economy.

Has the spread between HELOC and Mortgages rates ever looked like this?

There is less than a .5% difference right now between here is money to buy a house (mortgage) + here is cash to do whatever you want with it (HELOC).

The era of free money and cheap money has passed. Those of us following this site for a while have commented several times that nobody with a 3% or less loan would have any desire to refinance. It’ll take a lot of down pressure on the market to get these folks to stop making payments so these loans will likely never see a refi. These houses will become rentals when people decide to upgrade and likely not get sold for a long long time. They’ll be some HELOCs and such but nothing meaningful from this market share for a while. Loan agents will be doubly hit by this downturn as well as the fact that a robot can do most of what they do. Anymore, a real estate site combined with a virtual loan assistant will put a lot of the real estate sector out of business. Escrow companies will be needed for much longer but in the short term they’ll be laying off folks really soon, too. Nothing good is on the horizon.

Not everyone has the luxury of buying a new home while renting the old one. I believe the vast majority of people are forced to sell, for job change or whatever other reason. Consider the fact that if people buy a new home, it will carry a mortgage rate of 6%+.

With today’s regulatory environment, I don’t know if this is still even possible, but my grandfather did something interesting back in the 50s.

He provided mortgages (slightly undercutting banks) out of his own pocket.

This was when a new atomic facility was built nearby. The influx of people with guaranteed decent incomes was huge. He never had one single default. He helped out many people and made good money doing it.

My pockets ain’t deep enough to do that. But, it makes think about current times. There’s always something going on somewhere that’s going to provide (pretty much guaranteed) for folks somewhere. They might have to move, but they will.

If you know where that place is, and you have the money, it could be quite the opportunity.

That said, there’s still the current day issue that RE is way overvalued. Big monkey wrench there.

Nevertheless, there’s always an opportunity hiding in bad times.

People with enough money to buy multiple houses don’t get into the lending business; they get into the landlording business.

This is definitely somewhat more-true now than it was in the 1950s. Nationwide, computerized, oligopolized credit ratings are a huge part of that. Renters were a risk, but a mortgagee can’t abscond with the land.

Back then, your “credit rating” amounted to taking off your hat and convincing grandpa that you were a God-fearing family man — and that you verifiably had a job at the boom boom plant.

I can see using a lease option over 30 years. Pay me every month on time and I’ll give you this house. If not, even one month late and you must leave and I keep the money.

Well, best of luck to you, but I hope the good Lord never entrusts you with too much money.

The Rent-to-Own agreement is nothing new. Scum-bag landlords aren’t either.

Not to let scum-bag tenants off the hook either.

Long term lease with immediate surrender upon default in the far distant past was called a vive-gage, Latin for a live hand (holding onto the land) rather than a mort-gage, dead hand. Or so I’ve read.

Most private loans these days are 5 years, 15 years tops. Mostly to investors and also to people buying homes which can’t pass any bank inspection, or land. They were at 10% last I checked, probably higher now. Banks are at 11% for personal loans. At least in my area.

It’s fairly common (or used to be) in my area for people to buy a fixer with a large down and a private loan which gets transferred into a mortgage or equity loan when it is able to pass bank inspection. The private loan is often a killer as it’s short term compared to mortgages.

For the companies they did not creat the process or the Fed. Mtg brokers know their business is just a few interest rates hike from being eliminated which happened and I assume eyes wide open during the reckless Fed days.

I still think a lot of the housing pain won’t be distributed but will be centered in the cities highlighted by many of Wolf’s Atticus’s of the inflated housing prices the last 2-3 years. Interest rates from the Feds now have a Canadian model to pursue but are reluctant to lead the race in QT. Sept has the 95 billion to roll off!

What ever happened to Network Capitol Funding, located right in Wolf’s back door of Irving California??? . They were on the air on our local station here for 7 years on Sat at 1PM. Suddenly, they were replaced by some stupid talk show garbage.

“For whom the Bell Tolls” That is not the case today. Current borrowers, on average, owe just 42% of their home’s value on both first and second mortgages. It is the lowest leverage on record. Losing some value on paper shouldn’t affect those owners at all. (Early Adapters took Advantage of QE)

There are, however, about 275,000 borrowers who would fall underwater if their homes were to lose 5% of their current value. More than 80% of those borrowers purchased their homes in the first six months of this year, which was the top of the market. (Late Arrivals to the Dance). All good things come to end. Can’t get blood from a turnip. Nobody’s lining up for the 6.5% all you can eat mortgage buffet. Seem more and more lining up for QE haircut and shave special….

The last 75 years have literally been The Age Of Inflation. A relative bought a house in San Marino, CA, in 1975 for $57k cash…..at the time, no bargain. Prop 13 grandfathered in minimal pty tax increases. Zillow Zestimate is now $3.2 million. No matter when you buy in the real estate cycle, if you pay cash and hold the RE long term, you will have a roof over your head and inflation proof your wealth. Bonds, bills, and CDs are sucker bets with actual inflation far exceeding any return. Buy RE with cash, live in it, enjoy it, never ever mortgage it, and hold on to it if you can…..it sure beats a blue tarp or a tent.

Timing is everything

Zillow estimate 😀

A lot of readers come here for good insights, unfortunately your comment is not one. It is simply insane for majority of people to not leverage the bank when the *real* interest rate is negative. Specially more in real-estate tax friendly countries (most 1st World countries), where you can apply deductions/amortizations on 100% of your house value, and not only on your down payment.

What a crazy world for the Fed! CPI still above 8%, EFFR still below 2.5%. The stock market shooting up, making the Fed want to tighten harder, while the mortgage market, the lifeblood of the economy, is collapsing and making the Fed want to ease. Meanwhile, other Central banks are hiking 0.75%, so the Fed feels compelled to hike 0.75% at its next meeting to cover them. They might switch to the magic eight ball as a monetary tool.

Is it my imagination but airfare has been falling?

Round trip from my city to NY is usually $250 to $300. in October i can find round trip tickets at $160 to $200.

Maybe it is just the time of year?

I work for a private real estate investment company and we’ve had a moratorium on leasing office space to mortgage brokers for the past 12 years. In my boss’s words ‘they’re the first ones to throw the keys at you’ when their business slows down. Suffice to say the default rate is much higher on average than other small office tenants ie CPAs, Lawyers, Psychiatrists, etc.

Your email address will not be published.

“Housing market is pulling back as anticipated, following unsustainable growth during the pandemic.”

In terms of diversification between stocks and bonds, there is none. Not anymore. They even nailed the bear market rally in lockstep.

Never a boring day in the SPAC & IPO hype-and-hoopla clown show.

The Fed’s big liabilities: reserves, US paper dollars, RRPs, and the US government checking account. Reserves already plunged by $1.03 trillion.

Interesting stuff happening in the labor market, suddenly.

Copyright © 2011 – 2022 Wolf Street Corp. All Rights Reserved. See our Privacy Policy

Powerful Wealth Building Resources